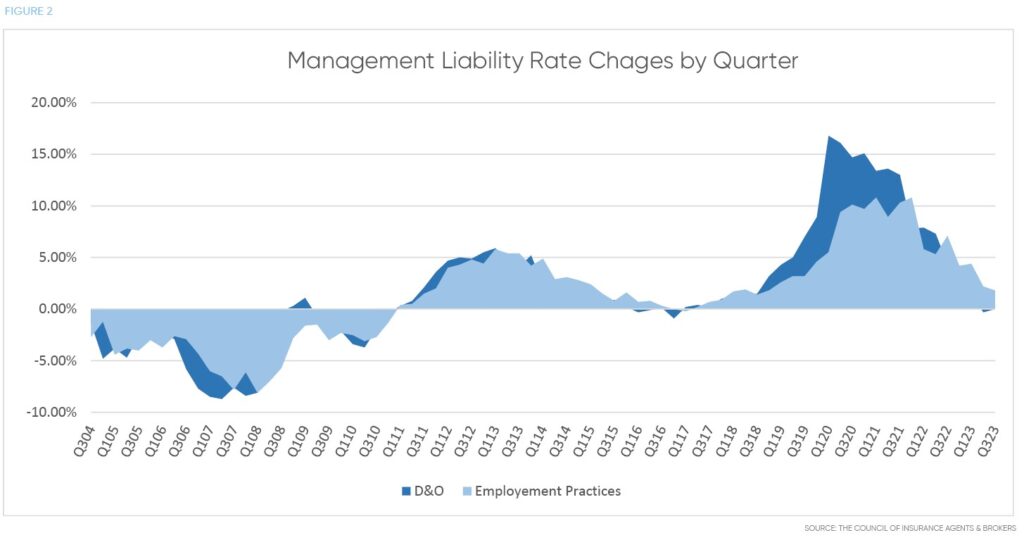

EPLI Projected to Tighten Amid Ups and Downs

Over the past five years, the management liability market has been in a state of flux, with carriers trying to navigate social inflation alongside volatile economic conditions. This has led to swings in rates, market capacity, and underwriting demands. While there was an increase in new players entering the market in 2021 and 2022 to take advantage of lower than expected losses, we expect rate, capacity, and underwriting to tighten in the coming year.

This report will provide perspective on the reasons behind these trends as well as a look over the horizon regarding some of the potential expected headwinds and the advisement businesses will need in place.

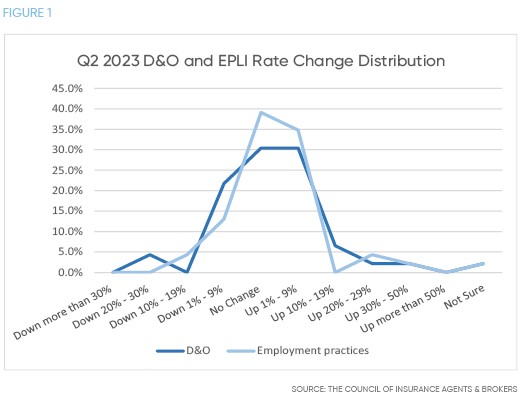

EMPLOYMENT PRACTICES RATE RECAP

Employment practices liability insurance (EPLI) has historically followed a similar trend line with directors and offers (D&O) insurance when comparing rate change. Substantial macroeconomic shifts often impact risk and rates in both lines of business, albeit for different reasons. A recession may cause market tightening on the D&O side for financial viability considerations, while also posing a challenge for EPLI due to the resulting layoffs that generate lawsuits over wrongful terminations.

The COVID-19 pandemic prompted carriers to take a cautious approach to EPLI with more restrictive appetite, terms, and pricing as reflected in the dramatic rate increases from 2020 to 2022. While COVID-19 claims did materialize, the impact was less pronounced than anticipated, and EPLI rates have since waned and stabilized—at least for the time being.

EMPLOYMENT PRACTICE TRENDS

The post-pandemic landscape has introduced a multitude of challenges and new exposures for employers. The power dynamic has tilted in favor of employees, prompting employers to rethink talent retention and attraction strategies, resulting in the work-from-home/return-to-office tug of war. Training and timekeeping in a remote work environment poses hurdles for employers, necessitating diligence in employee development and consistency with policies and procedures that are updated to align with the realities of remote work.

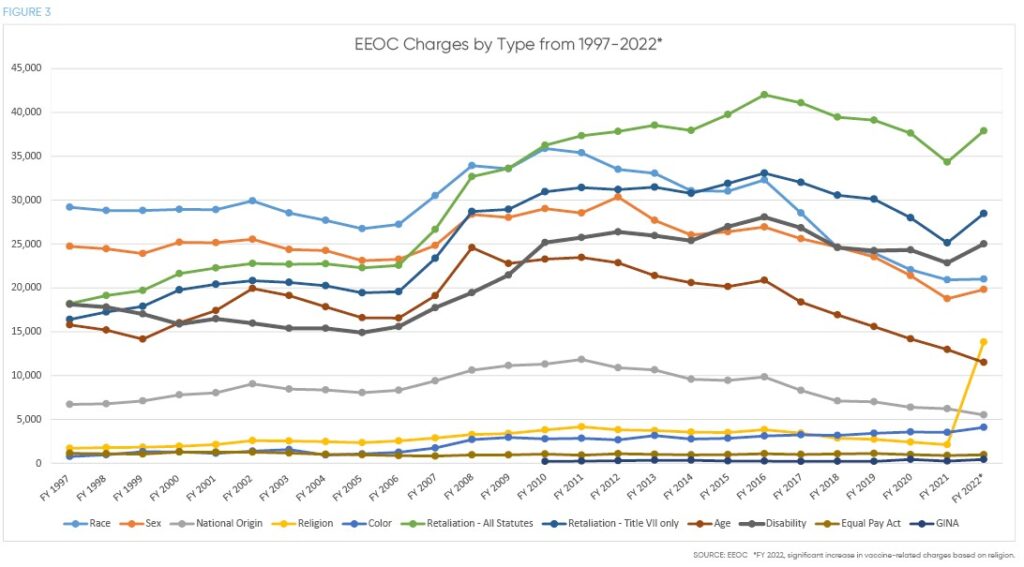

On the flip side, as people return to the office, accommodation demands have expanded beyond traditional requests, including considerations for immunocompromised individuals, mental health, and long COVID. The increase in in-person interactions also led to a rise in Equal Employment Opportunity Commission (EEOC) claims in 2022.

This significant shift is particularly noteworthy as it marks the first increase in discrimination charges since 2016. Religious discrimination, in particular, experienced the most substantial surge in claims. The EEOC, in acknowledging this trend, stated, “In 2022, there was a significant increase in vaccine-related charges filed on the basis of religion. As a result, 2022 data may vary compared to previous years.”

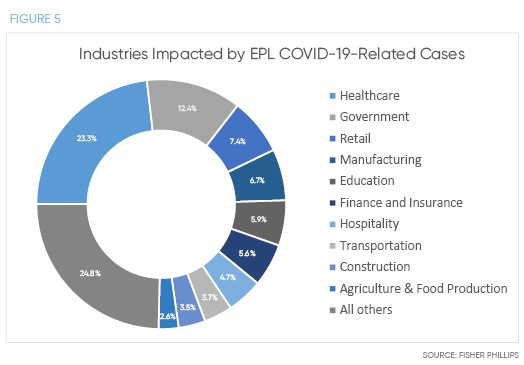

While COVID-19 may seem to be in the rear-view mirror, the number of lawsuits against employers continues to rise, with over 2,400 cases filed in 2023 alone, according to the Fisher Phillips COVID-19 Employment Litigation Tracker. Employment discrimination is the leading type of claim, with vaccine, retaliation/whistleblower, and remote work close behind.

Some states are having outsized troubles in the EPLI market, with carriers taking a very conservative approach to overall EPL coverage in California, Florida, and New York. In difficult states—characterized by frequent or large class-action or mass tort claims—carriers are seeking to limit exposures by increasing policyholder retentions or requiring separate retentions for highly compensated employees, something to monitor when purchasing coverage.

Additionally, classes of business where staffing is transitory and turnover is high—particularly healthcare, hospitals, hospitality, retail, and schools—as well as individual businesses with poor loss history can expect difficulties in placing insurance.

HEADWINDS AND HOT BUTTONS

EEOC

In its role as the federal agency responsible for enforcing laws that prohibit workplace discrimination, the EEOC is tasked with examining complaints tied to protected classes, including race, religion, sex, age, disability, etc. If a violation of the law is identified, corrective actions are pursued either through agreements with employers to modify workplace conditions or through legal action against the employer.

The EEOC promises to be an active litigant in upcoming years, as is evidenced in its strategic priorities for fiscal years 2023-2027, which include:

- Eliminating barriers in recruitment and hiring

- Protecting vulnerable workers and persons from underserved communities from employment discrimination

- Addressing selected emerging and developing issues

- Advancing equal pay for all workers

- Preserving access to the legal system

- Preventing and remedying systemic harassment

Artificial Intelligence (AI)

At the forefront of many conversations around technology is the implementation and utilization of artificial intelligence (AI). The public release of ChatGPT succeeded in highlighting how far this technology has come. Today, AI has evolved to permeate nearly every industry and operational infrastructure. As machine learning algorithms gain prominence in employment processes, concerns about the inherent biases have emerged. Initially seen as a tool to combat biases in hiring and employee-related decisions, machine learning algorithms can inadvertently perpetuate historical biases present in their training data.

In an unprecedented settlement, on August 9, 2023, the EEOC settled its first AI discrimination lawsuit with iTutorGroup agreeing to pay $365,000. The EEOC claimed that iTutorGroup programmed its application review software to reject applicants based on age. While this circumstance was unique because the defendant utilized proprietary software, it raises the question of potential liability for companies using third-party software with similar shortcomings.

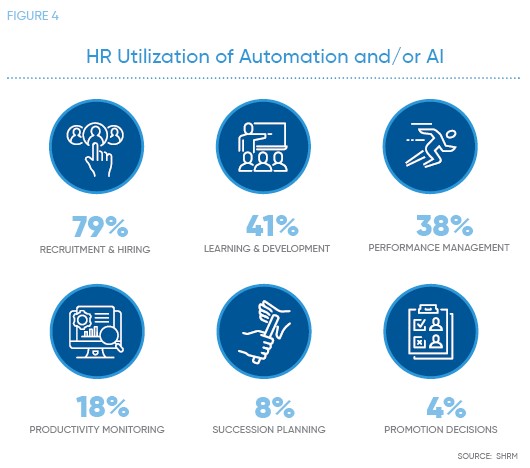

This case, amid increasing EEOC warnings of AI-related discrimination, serves as a crucial reminder for employers to ensure AI use in employment decisions is nondiscriminatory, particularly in recruitment, where approximately 79% of employers incorporate AI.

Biometrics

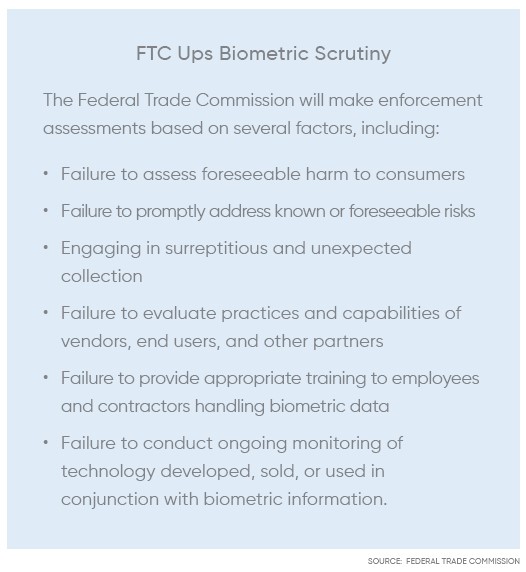

Biometrics is another trending area where employers need to be wary. The Federal Trade Commission is targeting unfair or deceptive acts as well as consumer privacy, data security, and bias/discrimination resulting from biometric data collection, storage, and use. This technology is widely used in business and includes fingerprint, palm, or iris scans; facial and voice recognition; genetics; and descriptions, images, recordings, and other data that identify an individual.

In response to state laws that regulate collection, storage, and use of biometric information, employment practices lawsuits have been filed. Notably, in February of this year, the Illinois Supreme Court ruled that a violation of the state’s Biometric Information Protection Act (BIPA) occurs every time an organization scans or transmits a person’s biometric information, meaning businesses that use biometrics on a continuous basis could face devastating financial consequences. Some carriers are taking action to limit or exclude coverage as a result.

ON THE HORIZON

Often business owners are concerned primarily with insurance rates. As it stands, the most recent data indicates nominal rate increases for the majority of EPLI risks. That said, the future is understandably uncertain.

With qualified labor shortages persisting and the Federal Reserve’s Open Market Committee declaring in June that it expects decelerating real GDP growth followed by a U.S. recession, companies may face substantial performance problems. Businesses can expect a credit squeeze, tougher standards to qualify for loans and letters of credit, and pressures on liquidity, all while workers demand higher pay to cope with ballooning interest rates and consumer prices.

Limits on hiring and pressures to downsize staff are intensifying, and the percent of the workforce holding multiple jobs continued its rise in October to 5.2%, according to the latest data from the St. Louis Federal Reserve. Such economic stressors can lead to complaints over wages and hours worked, unfair hiring and firing, and employers neglecting quality of working conditions.

Amid all of this economic turmoil, an astounding 90% of companies with office space plan to return to the office in 2024, and an alarming 28% stated they will threaten to fire employees who don’t comply, which threatens to drive up EPL claims and costs.

WHAT ARE CLIENTS TO DO?

IOA’s in-house management liability experts partner with our brokers to help clients navigate the turbulent waters of the D&O and EPL insurance marketplace. Our dedicated specialists keep abreast of regulatory and carrier changes and make sure business owners have the help they need to find coverage options that fit their risk exposures and financial strategy. For more information or to begin a conversation, reach out to your IOA advisor.

For a full copy of the Focus Report: EPLI Market Outlook 2023, contact IOA Management Liability Practice Leader Michael McLaughlin at michael.mclaughlin@ioausa.com.