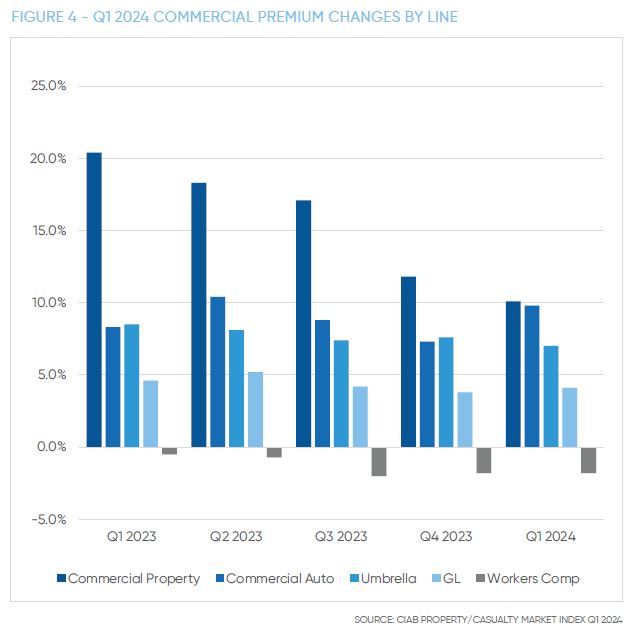

The biggest insurance issues for commercial property owners remain cost and availability of coverage. Commercial property premiums rose an average of 10.1% in first quarter 2024, according to the latest data from the Council of Insurance Agents & Brokers (CIAB). That was down from 11.8% in fourth quarter of 2023 and 17.1% in third quarter of 2023 but was still the highest premium increase across all lines of business, the CIAB Property/Casualty Market Index Q1/2024 report said.

As prices have risen over the past couple years and insurer losses have become more manageable, new real estate insurance capacity has entered the marketplace—either through the emergence of new program managers or carriers or due to an increased willingness of reinsurers to backstop traditional carriers in the real estate sector. That said, in states hit hard by hurricanes, flooding, and wildfires, insurers have shuttered operations, leaving a dearth of options in these areas, even for those who have not had claims. Government markets of last resort are available but have less than optimal coverage, and prices are going up there as well.

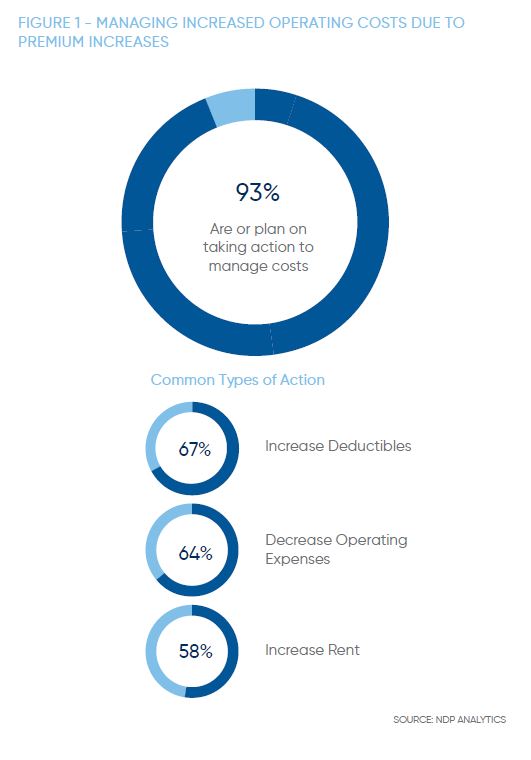

To control premiums, clients are having to take on more of the risk they’re exposed to. This appears in higher deductibles, higher self-insured retentions, and higher attachment points for excess insurance. Property owners also are expected to take mitigation measures—sometimes costly—to qualify for renewals or new coverage.

Properties with an unfavorable loss history or in vulnerable areas for natural catastrophes—hurricanes, tornadoes, and hail especially—are experiencing major increases in premiums coupled with spikes in retentions and deductibles. These clients need to come to the table with serious evidence that their properties are hardened against perils, preferably verified by a third party. They can expect wind and hurricane deductibles in the 5% or higher range. Without those deductibles, premiums are through the roof.

spikes in retentions and deductibles. These clients need to come to the table with serious evidence that their properties are hardened against perils, preferably verified by a third party. They can expect wind and hurricane deductibles in the 5% or higher range. Without those deductibles, premiums are through the roof.

Older properties and those with frame or jointed masonry construction also struggle to find quality, affordable coverage terms.

Much of the burden for controlling premiums—and getting quality coverage and terms at all—rests on clients and brokers, who must come to the table prepared with solid evidence that loss-control efforts are in force. Insurers demand top-quality data, especially on valuations and repair and replacement cost estimates. Many carriers want to see third-party validation of valuations, such as Marshall & Swift cost breakdowns of replacement, depreciation, and component costs. Co-insurance and underinsurance penalties are being enforced at claim time for accounts that fudge the numbers.

TRENDS & COSTS

To best address the real estate market, we’ll look at several important segments and their major lines of coverage.

Multifamily Habitational

The standard market for insurance coverage in multifamily habitational is tight, especially for frame construction, apartments built before 1995, and coastal properties. Many clients are being forced into the excess and surplus market. Both property and liability coverages are under pressure, and though premium increases are moderating nationwide for non-catastrophe exposures, clients can expect to see carrier reductions in coverage benefits. Additionally, availability of guaranteed cost policies is on the decline as carriers demand higher retentions for habitational properties. Large accounts are routinely seeing a baseline self-insured retention of $100,000.

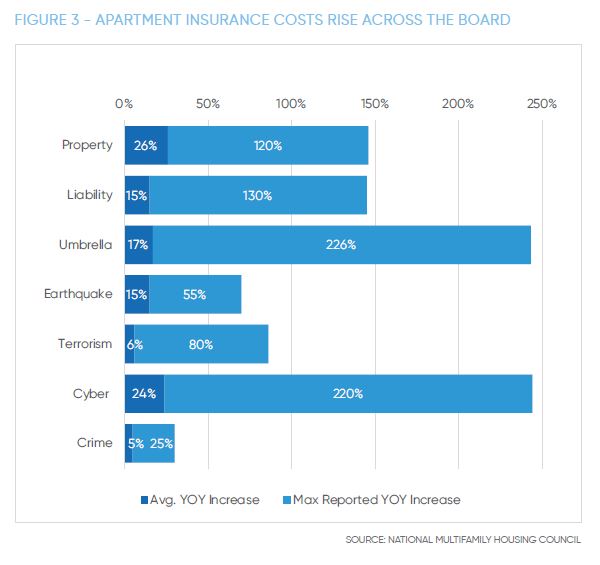

- Property insurance: Catastrophe-prone multifamily properties are experiencing the worst of the commercial property insurance problems. Premiums are up on average 150% since 2022 for large multifamily property coverage nationwide but even more for high-risk buildings. Sublimits on wind-driven rain incursion for coastal properties and sprinkler-caused water damage in earthquake-prone regions are common, and specific hail and wind deductibles are typical in coastal and high-tornado-risk areas.

Renewals and new coverage are receiving greater scrutiny than in years past. Beyond property upkeep to prevent leaks and other water damage, safety precautions are a central issue. They include updating electrical systems and HVAC, and maintaining and controlling sprinkler operations. Building records on maintenance and repairs as well as insurance company searches of resident complaints over building upkeep are part of the standard review. In the past, multifamily owners could absorb more in the way of deductibles, but today, with interest rate and inflationary trends, they are working on tighter margins. Multifamily owners are facing double-digit hikes in operational costs, so capital for residential services, upkeep, and insurance is challenging—sometimes unavailable. Hard choices have to be made, and uncovered risk is the result in too many cases.

Renewals and new coverage are receiving greater scrutiny than in years past. Beyond property upkeep to prevent leaks and other water damage, safety precautions are a central issue. They include updating electrical systems and HVAC, and maintaining and controlling sprinkler operations. Building records on maintenance and repairs as well as insurance company searches of resident complaints over building upkeep are part of the standard review. In the past, multifamily owners could absorb more in the way of deductibles, but today, with interest rate and inflationary trends, they are working on tighter margins. Multifamily owners are facing double-digit hikes in operational costs, so capital for residential services, upkeep, and insurance is challenging—sometimes unavailable. Hard choices have to be made, and uncovered risk is the result in too many cases. - Liability insurance: Slips and falls are still the most prevalent general liability complaint, but failure to prevent or deter crime is a rising concern for apartment and condo building owners. Violent crimes have remained elevated since 2019, with 24% more homicides in the first half of 2023 than H1 2019, according to the Council on Criminal Justice (CCJ). Though the CCJ reports rates of violent, drug, and property crimes (except auto theft) were down or stable in the first half of 2023, year over year, the organization says that violent crime is “intolerably high” in poorer sections of cities.

- Steps to improve resident and guest safety are crucial to preventing loss. In Florida, such measures were codified in March, and all multifamily properties are required to comply. Habitability claims based on subpar living conditions are growing in frequency and severity. As a result, insurers are adding implied habitability warranty exclusions to multifamily insurance policies. Definitions of habitability vary across states but typically include heating; clean, running water and working toilets; electricity; hot water; no mold; no pest infestation; and functional doors, locks and windows, among other safety essentials. City and county planners are emphasizing the need for mixed-use developments, which are often in densely populated areas. Resident and business safety are primary insurance and risk-management considerations. Several MGAs have opened in the last couple of years to cater to the mixed-use niche.

Affordable housing complexes face compounded problems because of riskier crime profiles, limited rents, and exclusions for resident injury liability. Insurance prices have escalated 103% over the past four years in the space, according to the New York Housing Conference.

Affordable housing complexes face compounded problems because of riskier crime profiles, limited rents, and exclusions for resident injury liability. Insurance prices have escalated 103% over the past four years in the space, according to the New York Housing Conference. - Senior housing is also suffering from high premiums, with a special focus on resident injury liability and employee-related risks.

Condominiums

Condo associations are experiencing the same tight market as commercial habitational. Accounts with a less than favorable loss history are finding it very hard to find coverage, and those without claims are still seeing upwards of 20% increases along with substantial deductibles for certain perils.

- Property insurance: Coastal condominium associations, especially in Florida, are seeing drastic increases in property insurance costs, in extreme cases rising more than 30%, even with deductibles doubling. Most property insurers require a roof replacement (not a roof update) of buildings every 15 years to ensure coverage eligibility. Appraisals need to be done every 36 months, and insurance companies are requiring engineering inspections and reserve studies in compliance with jurisdictional mandates.

- Liability insurance: Condo association liability for personal injuries, especially resulting from violence in common areas, is a developing—and potentially lucrative—field for the plaintiffs bar. We recommend all condo associations use security cameras and full lighting in common areas, and in Florida, we believe HB 837, which was signed into law in March, applies to condo associations. That law offers a presumption against liability for multifamily habitational properties that implement security measures, including carded-access locks on gates surrounding pool areas in addition to the security recording and lighting mentioned above. The liability of associations regarding individual unit owners’ fulfillment of security measures such as door viewers and window and door locks is something we are following.

Non-habitational Commercial

This broad category of real estate includes retail businesses, office parks and buildings, industrial and data complexes, warehouses, churches, and schools, among other property types. Owners need to protect not only their physical property but also their business assets from liability claims. Both property and liability losses are increasing, and insurers are responding with higher costs of insurance, limitations on or outright exclusions from coverage, and demands for more policyholder skin in the game.

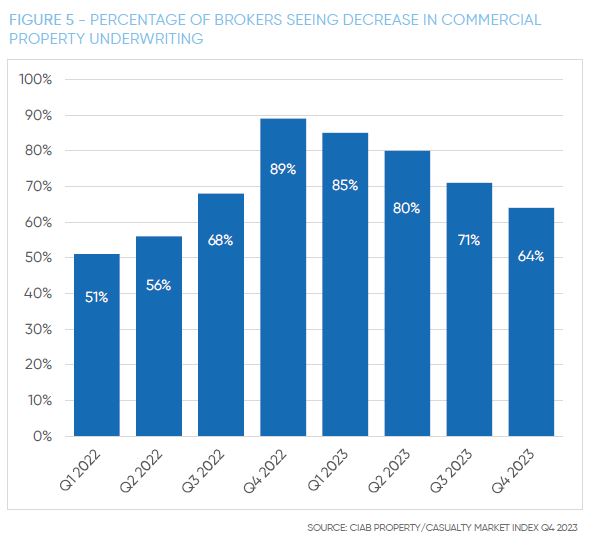

- Property insurance: Storm, wildfire, and strike, riot, and civil commotion (SRCC) exposures top the list of property claims, and insurers are responding by increasing premiums in areas prone to these loss events or pulling out of markets with these exposures altogether. Thirty-seven percent of brokers responding to the CIAB Property/Casualty Market Index Q1 2024 survey said they saw an increase in commercial property claims, though that’s down from 42% in the previous quarter. While commercial property premium increases slowed to 10.1% in the first quarter of 2024, capacity remains a problem. January 1 renewals indicated a split market, with pricing hikes moderating a bit, though still in the double-digits, for non-cat-exposed accounts. For catastrophe-prone regions, however, capacity is constrained, and prices and deductibles are high. Reinsurers are making more capital available, so property insurers do have more capacity, but carriers are being very selective in the risks they take on. Higher deductibles, higher self-insured retentions, and the use of multiple insurers to get to adequate levels of coverage are commonplace. Many accounts in wildfire, hurricane, earthquake, and wind/hail zones are finding sublimits or the need to go to the specialty market for those perils. SRCC rate increases were still in the double-digit range at the end of 2023, and with the college protests, anti-business property attacks, and upcoming elections, SRCC insurers will be evaluating the exposures on location-specific and commercial sector bases. Exclusions in all-risk policies or sublimits for SRCC losses are increasingly being applied.

- Liability insurance: Liability premium increases have moderated—changing up or down within a point across general liability and umbrella for the past four quarters. But attachment points for excess coverage are high, and insurers are keen to see risk prevention documentation. Additionally, insurers are dialing back on guaranteed cost programs and moving more accounts to loss-sensitive coverage. One noteworthy claims trend, especially in New York but also in Illinois and other states, is in third-party injury liability. “Action over” (or third party over action) claims for falls from heights during building maintenance or construction, in which strict liability is assigned to building owners and contractors, are a growing concern. Many insurers include an exclusion to prevent paying both an injured employee’s workers comp claim and that employee’s claim against a third party who is contractually indemnified by the injured worker’s employer. Contracts and insurance policies should be scrutinized to discover “action over” gaps.

Real Estate Investment Trusts

REITs have unique insurance needs in the real estate sector. Those include property coverage for commercial business property, multifamily complexes, as well as single family homes, which are a growing portion of REIT portfolios. REITs and other commercial real estate investors also face fiduciary and other liability exposures for the properties they own. REITs have seen some modest reduction in D&O rates over the past year, but they suffer from much the same rate pressure in property as other residential owners. Though double-digit increases, even in non-cat-exposed areas are not uncommon, some properties with lower insurance claims in low-risk areas reported minimal changes to premiums.

As for fiduciary coverage, investment losses are a key issue REITs are contending with as the value of non-habitational commercial property tanks and the cost of property coverage escalates. A volatile property market has led to financial concerns among insurers. Uncertainty regarding a potential future collapse in commercial real estate valuations has carriers increasingly concerned, resulting in conservative appetite, pricing, and coverage.

While apprehension previously existed regarding ballooning commercial property valuations, the impact of COVID and a shift to remote work escalated these reservations to unprecedented levels, and investors’ reactions are clearly driven by similar concerns. With redemption requests from real estate funds at or close to all-time highs, REITs have to focus on portfolio balancing, accurate valuations, and loan/disclosure accuracy. Fiduciary and D&O liability coverage are key.

SPECIAL CONCERNS

Construction

Builders risk insurance seems to have stabilized across most of the country, though rates are still rising and pockets of high-risk areas are experiencing both rate and capacity struggles. Non-admitted carriers are playing an important role, so brokers need to be prepared to access those markets, especially in coastal, convective wind, and wildfire regions.

High-risk projects can also expect higher deductibles, lower primary limits, and quota-share agreements for large projects. Mandatory wind deductibles continue. Some companies are securing private fire suppression companies in wildfire-prone areas, which can help demonstrate excellent risk mitigation.

New materials and construction methods, such as mass timber and modular units, are not that popular with carriers due to lack of claims history and performance data. Brokers will have to work to provide data that supports these accounts—maybe there’s an opening for quality artificial intelligence in this space.

Time to project completion is a key concern, especially with labor shortages and volatile supply chains. Keeping on top of renewals is very important, because insurer appetites are changing quarter to quarter based on losses and portfolio balancing. Building owners also need to be hyper-focused on accurate valuations for completed value, because insurers are going to enforce co-insurance rules for underinsurance. Inflation is a major component that must be factored in.

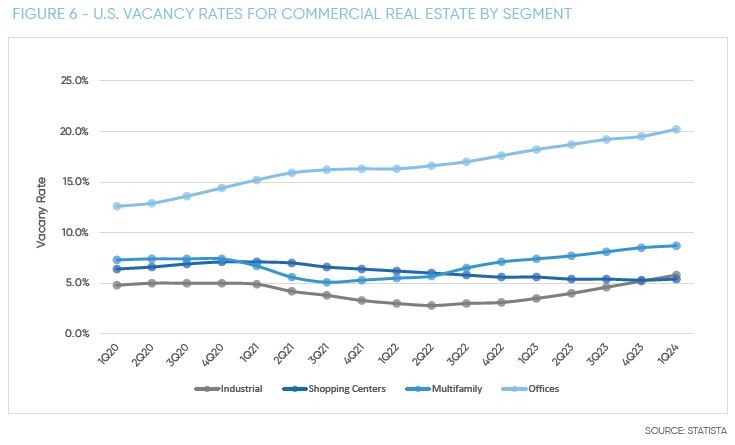

Vacancy

Vacancy rates are skyrocketing in the commercial office sector, with shopping center and industrial property vacancies also on the rise. Vacancy insurance needs to be reviewed to ensure coverage and loss prevention for properties that suffer high emptiness rates. Building owners may need to turn to the E&S market.

Cybersecurity

Building operational technology (sensors, safety alerts, locks, etc.) and internet-enabled property manager operations are growing exposures. A National Multifamily Housing Council survey in 2023 indicated more clients are interested in this coverage and need to find a way to improve cybersecurity to become more insurable at better rates.

Property owners must contend with a growing threat landscape for building systems as well as proprietary data. The good news is cyber insurance rates have normalized as the industry has matured. The one showstopper for coverage is lack of cyber hygiene, so all real estate clients need to demonstrate modern cyber protocols to protect machinery, processes, people, data, and assets.

ON THE HORIZON

Representations and Warranties

With the increasing sale of properties—both to investment companies and liquidations—there is a growing demand for reps and warranties coverage. Prices have come down as the product has become more popular, but retentions are high. Only around 5% of claims exceed the retention threshold, but those that do are very big and make the product well worth the time and effort. Claims typically focus on financial statements, condition of physical assets, and sustainability of contract relationships.

Construction Defects

As demand for housing grows, property owners need to be sure contractors have sufficient construction defect coverage. The number of claims is increasing, especially in the multifamily space, and some are substantial enough to trigger habitability lawsuits, rental loss, and vacancy clauses. As a result of the increase in construction defect claims—and in some cases massive judgments—insurers are pulling back from the space. It is important that property owners get full details on construction and product defect coverage for the builders they choose. With the ongoing shortage of skilled labor, knowing the builder well is important.

Surety

With increases in materials pricing, volatility in labor markets, a credit crunch, and a tight insurance market, some builders are abandoning projects. ConstructConnect’s Project Stress Index composite for the week ending May 13 indicates private-sector abandonment is about 34% higher than in 2021, while public-sector abandonment is about 20% higher. Both sectors have been improving this year, but project owners need a strong surety to evaluate contractors and protect owner assets.

Non-traditional Methods of Insuring

Managing general agents and managing general underwriters have been stepping in over the past couple of years to fill capacity gaps left by traditional insurers. These niche specialists, along with reciprocal exchanges, are particularly active in catastrophe-prone regions and may serve as good alternatives for accounts that are in coverage deserts. Private flood insurance is also more available to supplement shortfalls in National Flood Insurance Program coverage and is becoming much more mainstream.

Parametric insurance is also a robust field, especially for catastrophe claims and water-leak claims—exposures that can be sensor-monitored and instantly (or rapidly) measured. The coverage puts near-immediate cash in the hands of policyholders while other, more traditional coverage goes through the adjustment process.

COMPLEX RISKS NEED SPECIALTY CARE

In the complex world of real estate ownership and management, insurance solutions can make or break investment success. IOA maintains excellent relationships with admitted carriers, the excess and surplus market, MGAs/MGUs, and sureties that specialize in properties across all segments of the commercial property market. We help clients tell their best story to insurance providers and are experts at hard-to-place properties.

IOA-based risk assessments help property owners identify and control risks, and our specialists help prevent coverage gaps, meet valuation disclosure requirements, and assess contracts to make sure they align with insurance coverage for property and liability exposures. We coordinate with lenders, builders, and property managers and have claims specialists who assist with claim management.