Business insuranceInsightsRisk Management

Focus Report – 2025 Transportation Market Outlook

Written by: Staff Writer | May 1, 2025

Jump to section

01

Auto Liability Costs Are Major Pain Point for Transportation Companies

02

Trends and Costs

03

What’s Driving Insurance Costs

04

Notable Risk Factors & Mitigation

05

Novel Solutions

06

Serving the Complex Needs of the Transportation Industry

Auto Liability Costs Are Major Pain Point for Transportation Companies

The state of the U.S. economy remains the greatest concern for the transportation industry. Although small-fleet owners and trucking owner-operators indicated rising optimism in a fourth-quarter 2024 survey by Truckstop and Bloomberg, fraught tariff and trade negotiations with Canada and China may dampen that enthusiasm over the coming months. Moreover, the Cass Freight Index, which measures total freight expenditures, indicates falling shipment volume (a 5.5% year-over-year decrease in February), adding to the soft-market conditions in the for-hire sector emanating from the growth in private fleet capacity over the past few years, Cass Information Systems said in its February 2025 Index Report.

The regulatory environment is also a concern. Potential changes to regulations, including the U.S. Environmental Protection Agency’s trucking emissions standards, may introduce welcome relief, but the push to give states more authority may create a hodge-podge of rules, leading to industrywide complexity and confusion.

California regulations remain a top focal point. Efforts to curtail California’s mandates on truck manufacturers have had some success, with the California Air Resources Board in January pulling back on some electric vehicle (EV) mandates for fleet owners. EV concerns were, however, heightened by uncertainties over the ability to fuel electric trucks, as financing to build charging stations is on the list for budgetary cuts. Moreover, California officials have vowed to pursue other means to reduce diesel emissions, and about half a dozen other states have begun or finalized measures that follow California’s lead.

Outlays for fuel, repair and maintenance, loans, insurance, wages and benefits, and government-imposed fees—compounded by soft freight rates—are keeping average profit margins in the 3% to 5% range, according to financial modeling company FinModelsLab, and losses from higher or uncovered liability claims are a threat to bottom lines across the transportation industry.

This report looks at some of the drivers of insurance costs, a major concern of transportation companies, and what those in the industry can do to reduce their cost of risk.

Trends and Costs

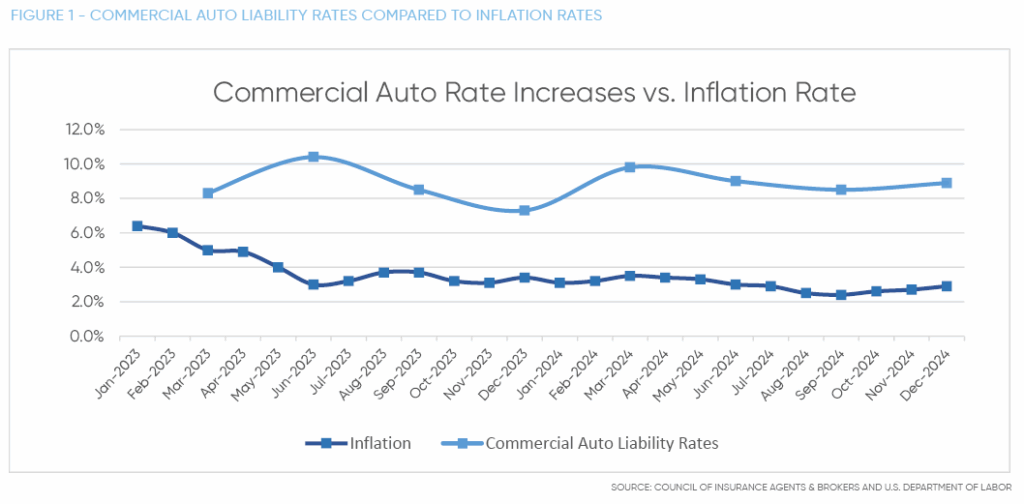

Though the overall economy ranks as the top concern of the transportation industry, insurance cost and availability rose eight spots, to number four, in the latest yearly roundup of critical issues in the trucking industry, published by the American Transportation Research Institute (ATRI) in October 2024. That corresponds with findings from the Council of Insurance Agents & Brokers (CIAB), which said in its Q4 Commercial Property/Casualty Market Index that commercial auto and umbrella insurance premiums rose the most of any coverage line: 8.9% and 8.7% respectively.

Though the overall economy ranks as the top concern of the transportation industry, insurance cost and availability rose eight spots, to number four, in the latest yearly roundup of critical issues in the trucking industry, published by the American Transportation Research Institute (ATRI) in October 2024. That corresponds with findings from the Council of Insurance Agents & Brokers (CIAB), which said in its Q4 Commercial Property/Casualty Market Index that commercial auto and umbrella insurance premiums rose the most of any coverage line: 8.9% and 8.7% respectively.

Auto liability costs may be reflective of two primary issues: lawsuit abuse and driver distraction.

Though Federal Motor Carrier Safety Administration (FMCSA) data for 2025 indicates higher than average crash numbers for fiscal year 2025 (beginning in October), driver distraction remains relatively low on the industry’s list of self-identified priorities: number 10, according to the ATRI survey.

What’s Driving Insurance Costs

Inflation

Inflation

Overall inflation eased in February, and the combined costs of commercial auto replacement parts and repair labor actually decreased 1.6% in the fourth quarter of 2024, according the latest Decisiv/TMC North America Service Event Benchmark Report, released in March. The authors suggest the cost declines resulted from greater stability in both supply lines and technician retention. But, while property costs may have decreased, liability costs have not.

Accident Frequency and Severity

National Safety Council (NSC) data indicates another year of increase in large-truck involvement in fatal crashes in 2022 (the latest year available)—to 5,837 from 5,733 in 2021, a 1.8% climb. The number of large-truck fatal crashes is up 49% since 2012. Both the 2022 and 2021 numbers far exceed the average since 2008, with no indication that COVID skewed that average. NSC data also show that there was a 2.5% year-over-year increase in the number of large-truck crashes that resulted in injury and an 18% increase since 2016.

Rural truck routes continue to log the highest number of fatal large-truck crashes, with 53.98% of the tally, versus 46.02% for urban travel. Daytime fatal accidents outweigh nighttime 61.3% to 38.7%.

Vehicle-related factors were related to 4% of large-truck crashes in 2021, according to FMCSA data, with tires and brakes the most common culprits.

Massive Penalties from Lawsuits

So-called “nuclear” verdicts—those exceeding $10 million after trial costs—are still terrifying insurers and transportation companies alike. For example, last summer, Wabash National was hit with a $462 million verdict after one of its truck’s trailer underride guards failed when a passenger car crashed into the rear of the trailer, leading to two fatalities. In another 2024 verdict, Daimler Truck North America was penalized $160 million in a rollover that paralyzed a man. A common complaint is that truck drivers and companies don’t need to be at fault in these lawsuits; the emotions of the jury are key.

Moreover, the lawsuits themselves can be extremely expensive, as litigation finance companies, which see huge potential sums from a victory, fund legal action as an investment, allowing plaintiffs—whether valid or abusive—to file and prolong lawsuits. The costs of defense can outweigh the cost of simply settling.

According to 2021-2024 data published by law firm Brown & Crouppen, the average truck accident settlement was $103,654. A Chubb 2024 benchmarking survey found that median insurance limits on insurance policies ran about $170 million in 2023 for the transportation/road sector but loss costs exceeded $450 million, indicating transportation companies are seriously underinsured.

Record Cargo Theft Losses

There was a 27% increase in the number of reported cargo theft incidents across the United States and Canada in 2024, according to CargoNet, with the average value per theft estimated at $202,364, up from $187,895 a year earlier. California and Texas are the hotbeds for cargo theft increase, at 33% and 39% respectively.

Raw and finished copper products, consumer electronics, and cryptocurrency mining hardware (computer products) were notable new targets CargoNet identified. Criminals’ top commodity targets were food/beverage and household goods. Trailer theft and burglaries were particularly problematic in major metropolitan areas, though warehouse/distribution centers and truck stops were the primary locations where theft occurred.

Notable Risk Factors & Mitigation

While concern over the economy scored about 30% higher than all other issues in ATRI’s 2025 survey, adequate parking ranked the next-highest concern. Drivers dominated the field in terms of the number of categories of concern, with compensation, shortages, and distraction all falling within the top 10 issues across drivers and motor carriers. Transportation companies continue to look for cost-efficient means to prevent losses and minimize hazards, but margins are tight and many expenses are beyond company control. That makes the few areas of loss they can control more important than ever.

While concern over the economy scored about 30% higher than all other issues in ATRI’s 2025 survey, adequate parking ranked the next-highest concern. Drivers dominated the field in terms of the number of categories of concern, with compensation, shortages, and distraction all falling within the top 10 issues across drivers and motor carriers. Transportation companies continue to look for cost-efficient means to prevent losses and minimize hazards, but margins are tight and many expenses are beyond company control. That makes the few areas of loss they can control more important than ever.

Drivers

While the availability of qualified drivers fell on ATRI’s scale of concerns to its lowest in 20 years (ranking at number nine of 10), ATRI suggests this is because the need for drivers also has fallen as freight hauling demands have dropped. But an economic turnaround would likely elevate this priority, especially since there is still an estimated shortfall of 60,000 drivers.

Training and monitoring of drivers is considered paramount in risk mitigation.

“Speeding of any kind” was the most frequent driver-related factor in fatal large-truck accidents, according to the FMCSA. Distracted driving was the second most common driver-related factor in large-truck fatal accidents, with FMCSA 2021 data indicating 4.9% of such crashes involved at least one driver distraction, while 4.2% involved at least one impairment. Driving under the influence accounted for 2.1 percentage points of impairment-related fatal crashes, while falling asleep or being fatigued accounted for 1.1 points of the 4.2% total.

Telematics, which measures driver behaviors such as speed, sharp turns, and hard braking, is still having trouble taking off or becoming a primary solution for mitigating driver-related accidents. High driver turnover means by the time an insurance policy is ready to be renewed, the data from the telematic devices may be irrelevant. Additionally, the cost of implementation is often not offset by savings on insurance or accident payouts.

One solution that may see better results is the installation of dashcams and other vehicle cameras—side-view, front- and rear-facing, and cabin interior. These often capture the events surrounding a crash, theft, or vandalism, which may help truckers avoid liability or recoup damages in the event of a first-party property claim.

Equipment Failure

ATRI’s Crash Predictor report of 2022, the latest available, says more than 73% of all driver/vehicle violations were associated with vehicle equipment. Personal injury law firms are hyper-focused on the topic, citing brakes, tires, missing or faulty safety equipment such as underride guards, lighting malfunctions, and transmission failures as top liability issues.

Maintenance is a time-consuming effort, but it is a knowable cost of doing business and one that can significantly reduce accidents and liability lawsuits. Moreover, truckers’ Inspection Selection System (ISS) scores—an FMCSA safety ranking that flags less safe trucks for roadside inspection—can affect trucking insurability and rates. Doing a regular review of the ISS score and improving it can save transportation companies on pull-in delays, costs associated with citations, and accident-related payouts.

Cargo Theft

With 2024’s record cargo theft losses, transportation companies must take measures to reduce their risk and liability. It’s worth taking a quick look at the types of theft and actions companies can take to reduce their vulnerability.

Theft from unattended trucks: Drivers must take precautions if they’re leaving their vehicle unattended for more than a few minutes. Theft of cargo from unsecured locations can be prevented by proper locking, parking that prevents access through loading doors, and alarms. Recovery efforts include GPS tracking of trailers and high-value cargo and use of vehicle cameras.

Fraud-based theft: This includes fictitious pickups, double-brokering scams, and identity and account fraud, among other criminal strategies. Verification is key to preventing these crimes. That includes background checks on employees and partners as well as confirming change requests through a known source—and making sure all employees follow through on these practices. Even with such efforts, spotting imposters is difficult since they are often linked to organized crime groups that have illicitly purchased motor carrier numbers. There are security companies out there specializing in verification, and they are worth considering.

Bill of lading falsification: Often done by miscreant employees in the supply or logistics chain, the alteration of bills of lading is often not detected until an inventory is completed after delivery. Load-tracking and freight-matching software or services can help ensure shipment integrity from pickup to delivery.

Cyber theft: This is the hardest to combat because of the sophistication of criminal exploits, but protecting against infiltration of company systems can begin with awareness of phishing, impersonations, and funds/cargo misdirection. Multifactor authentication and 100% verification of network access, system use, and driver and payment instructions are two of the most basic steps that all transportation companies should implement immediately. Protecting access credentials is paramount.

Tariffs

With the value of transborder freight flows in North America rising 20.8% between 2021 and 2024, according to the U.S. Bureau of Transportation Statistics, tariffs are a major concern for trucking, which accounts for 64.4% of transport modes. The Trump administration’s tariff policies may heighten the value of cargo and, thereby, the need for increased limits of insurance. Additionally, President Trump signed an executive order in February eliminating de minimis treatment for products made in China, meaning even minimally priced items from China will now reflect the cost of tariffs in their price tags. This will heavily affect last-mile delivery companies and may increase trucking cargo insurance pricing. The change also affects clearance processing time at ports of entry and could lead to significant delays on consumer goods.

Parking

The truck parking shortage poses notable safety risks for transportation companies, raising the potential for accidents, cargo/rig/trailer theft, and driver injury. It may also lead to violations in driver hours. ATRI suspects Truck Parking Information Management Systems (TPIMS) may be part of the solution, and it is commissioning a study of drivers who use TPIMS to see if they improve access to appropriate parking. TPIMS integrates highway signage, Department of Transportation websites, and vehicle or phone apps to assist truckers in finding designated parking.

Novel Solutions

As transportation companies seek ways to control insurance and loss costs, a few tenable solutions have emerged or are being perfected: the use of captive insurance, technology, and analytics.

Captives and MGAs

Last-mile deliveries comprise 53% of total delivery costs, according to Contimod data, and the compound annual growth rate for the North American market is projected at 9.68% through 2034, according to Precedence Research. Insurance capacity for delivery service providers (DSPs) has dwindled due to excessive liability exposures, and programs that were affordable are seeing 100% to 200% rate increases. As a result, cargo transporters are looking for alternative insurance sources of coverage. Captive insurance allows DSPs to contain insurance costs and enjoy substantial benefits from safety programs. IOA targets DSPs that have three or more years in the business with at least 25 vehicles in service.

Across all transportation sectors, managing general agents (MGAs) have become another stable source of capacity as traditional insurance companies have pulled back from loss exposures. If a transportation company has a reasonable safety record and someone who knows how to shop its insurance, finding affordable coverage should not be that problematic.

Safety/Efficiency Technology

Insurers review accident data to determine circumstances, fault, and claims costs. In addition, recent updates to the FMCSA’s Crash Preventability Determination Program expand the historical time frame for federal investigation of accidents as well as the categories of commercial truck accidents eligible for review. These reviews play a central role in plaintiffs’ lawsuits against transportation companies and carry substantial weight with juries. The need for independent data, such as that from vehicle cameras and telematic logs, is rising, and some insurers require such technology for placement of coverage. Other technology, such as routing and scheduling software, regulatory compliance programs, and cargo/carrier verification also are key to loss prevention and legal defense.

IOA Analytics

IOA provides a risk assessment to transportation clients to help them understand and prioritize loss control efforts. Our analytics address drivers, fleets, claims, losses, and the overall insurance program to identify pain points, risk exposures, and opportunities for improvement.

Serving the Complex Needs of the Transportation Industry

With economic and trade policy in flux, changes to insurance and safety regulations at the state and federal level, and the upward trajectory of liability insurance premiums, transportation companies need the expert care of specialists in both property and liability insurance. From reefer breakdown coverage to injury liability across state lines, IOA knows the transportation industry and can help find appropriate insurance for owner-operators, busing companies, and motor carriers of all kinds.

Our safety reviews and risk management services help your company keep losses to a minimum, making it more likely you will get good rates and terms on insurance.

To request a copy of the full report, email marketing@ioausa.com.

Written by

Staff Writer

|May 1, 2025

Jump to section

01

Auto Liability Costs Are Major Pain Point for Transportation Companies

02

Trends and Costs

03

What’s Driving Insurance Costs

04

Notable Risk Factors & Mitigation

05

Novel Solutions

06

Serving the Complex Needs of the Transportation Industry