Business insuranceInsightsRisk Management

A Year of Ups and Downs Ends in Stability for Most Lines of Coverage in 2024

Written by: Staff Writer | April 3, 2025

Jump to section

01

PREMIUM PRICE CHANGES – BY SIZE

02

PREMIUM PRICE CHANGES – BY LINE

03

NOTEWORTHY LINES

An overview of The Council of Insurance Agents & Brokers’ Commercial Property/Casualty Market Index Q4/2024 and marketing conditions ahead.

Each quarter, The Council of Insurance Agents & Brokers releases its Commercial Property/Casualty Market Index. Here, we review the 4Q 2024 findings, which utilize data from October 1 through December 31, 2024. We also consider current conditions to provide context for risk transfer solutions and strategic planning for emerging risks.

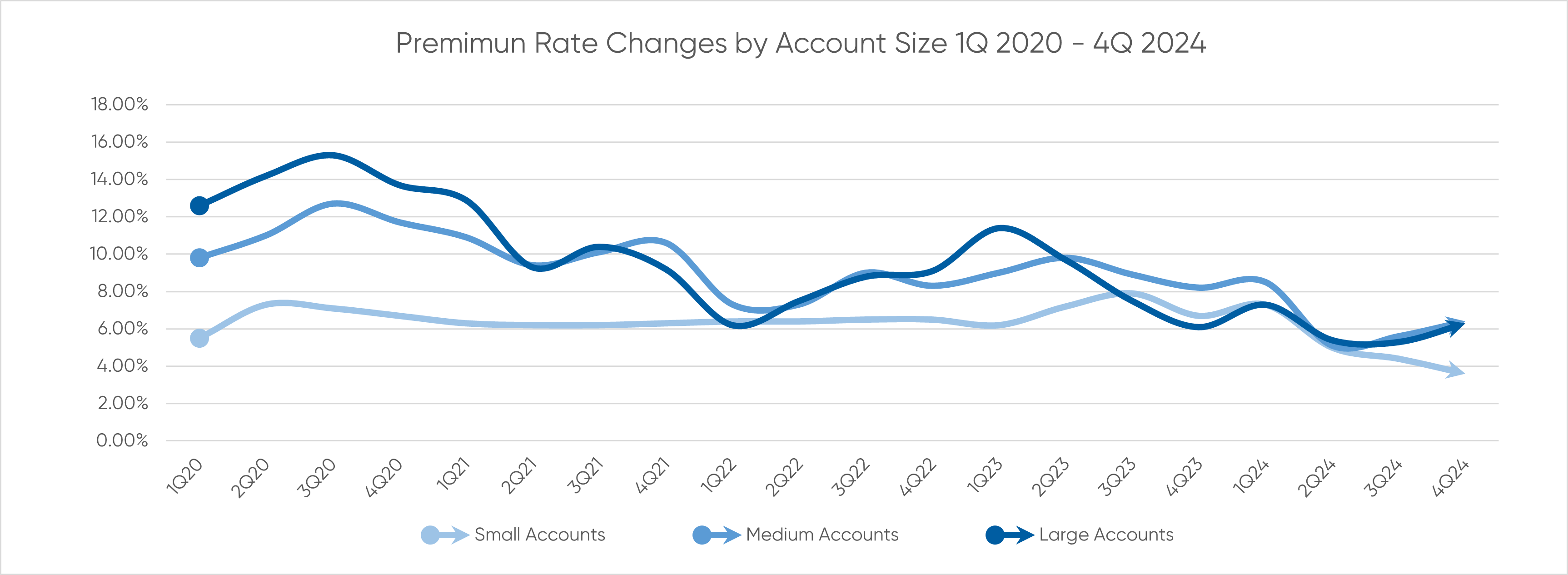

PREMIUM PRICE CHANGES – BY SIZE

Market conditions remained fairly predictable throughout the course of 2024. In the last quarter, commercial lines premiums increased for all account sizes just slightly above the previous quarter at 5.4% on average. This marked the 29th consecutive quarter in which premiums increases were seen across all account sizes.

Medium-sized accounts once again saw the largest increases at 6.4%, followed only slightly behind by large accounts at 6.3%. Small accounts saw some welcome relief coming in at 3.6%, down from 4.4% the previous quarter. According to one firm, the appetite for small business accounts remained strong, and others noted that medium and large accounts saw rates remain status quo, despite some reporting more information requests and less capacity.

PREMIUM PRICE CHANGES – BY LINE

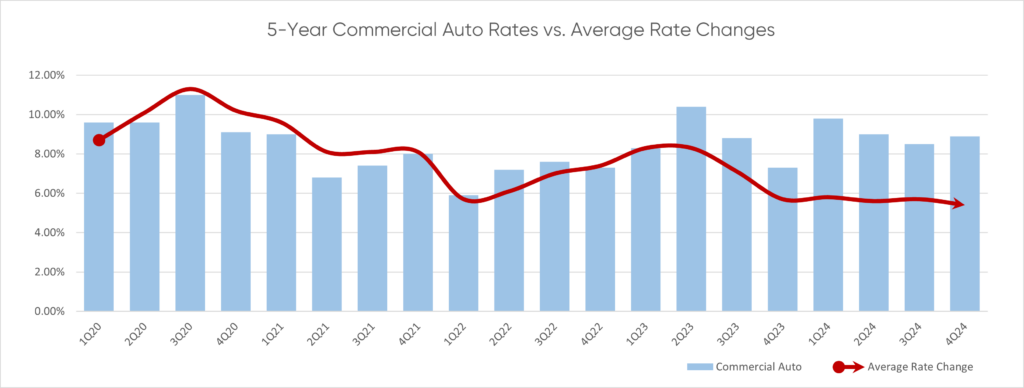

Two lines of coverage experienced the highest premium rate increases this quarter. Commercial auto came in on top at 8.9%, and umbrella followed closely behind at 8.7%, representing the fourth quarter of increases for the line.

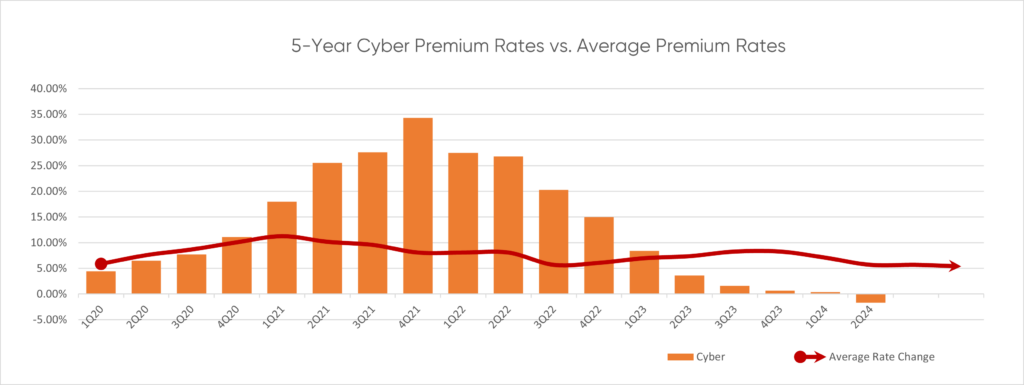

Conversely, employment practices joined the group of coverage lines in which premium rates fell, including cyber, D&O, and workers compensation, all of which continued their downward trajectory.

For other coverages, premium rate increases were similar to the previous quarter or came in slightly lower. One respondent perhaps captured it best by stating that it was “a stable quarter.”

NOTEWORTHY LINES

Commercial Auto

Since mid-2011, or for 54 consecutive quarters, premiums have been on the rise for commercial auto. In a November 2024 report, AM best stated that the average loss per commercial auto claim had doubled since 2014.

Cost drivers impacting market conditions were plentiful for commercial auto. Rising claims, higher repair costs due to vehicle technology, limit restrictions, and underwriting capacity decreases were noted as culprits in driving up rates. Commercial driver shortages and the upfront costs of moving to more electric-based fleets also were cited in the report as important factors impacting the market.

For example, fleet electrification in commercial and government organizations rose 233% from 2019 to 2021, according to Smart Energy Decisions. Insuring these vehicles can result in higher premiums due to their unique risk profile.

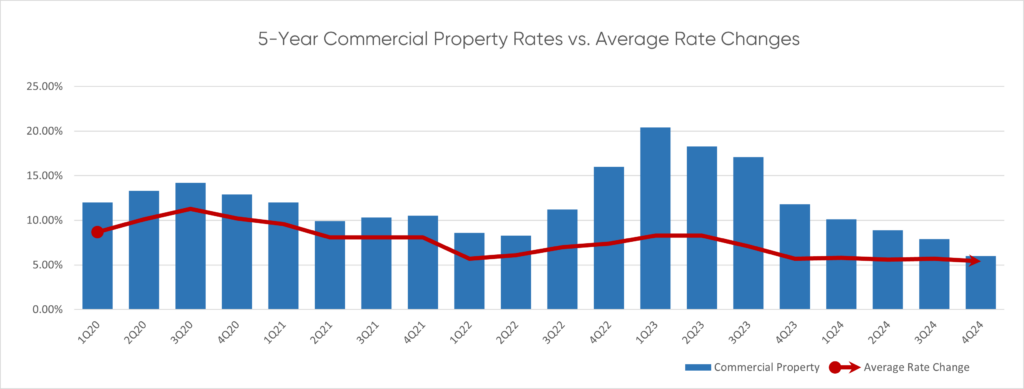

Commercial Property

With a 6% increase at the end of 2024, commercial property premiums continued their downward trajectory for the 7th consecutive quarter, down from 20.4% in 1Q 2023 and on par with 1Q 2019. While rates tend to vary wildly depending on property type and region, the overall trend here is promising.

Reinsurance may play a key roll in rate fluctuations in the coming year. While capacity has met demand, there are still threats on the horizon. The Insurance Information Institute in its latest brief, Commercial Property: Trends and Insights, stated, “The medium to long-term outlook for commercial property may hinge on whether the reinsurance market becomes more competitive in 2025, given the high frequency of catastrophe events and losses in the second half of 2024.”

Cyber

Cyber rates this quarter hit a record low at -1.8%, setting a second record for the line in 2024. Contributors to the trend in falling premiums were reported to be U.S. carrier competition and more underwriting capacity as well as improved cyber resiliency. This was the 3rd consecutive quarter the line experienced premium decreases.

Despite ransomware attacks on the rise, a key loss driver, downward pressure on the line persisted in the market. This was attributed in part to implementation of risk controls, which suggested “the focus on insured resiliency may be having an effect.”

According to CRC Group’s 2025 State of the Market report, “The average [ransomware] demand increased in 2024 to just over $2M, while the average payment was closer to $500K.” The report noted that in 2023, about three of every four ransomware demands were paid, which decreased to one in eight last year. The change was attributed to client investment in protecting backup systems and better cyber resilience overall.

Umbrella

Umbrella had the second highest average increase in 4Q 2024 at 8.7%, greatly lower than its peak average of 22.9% in 4Q 2020 but still significant.

MR Forecast’s report Commercial Umbrella Insurance 2025-2033 Trends: Unveiling Growth Opportunities and Competitor Dynamics noted that “considering the increasing frequency and severity of liability claims, coupled with rising corporate awareness of risk mitigation strategies, a conservative estimate would place the annual growth rate between 5% and 7%. Key drivers include escalating legal costs associated with lawsuits, the growing complexity of business operations leading to increased exposure to liability risks, and a rising demand for comprehensive risk protection among both SMEs and large enterprises.”

While moderation and stability have been used to describe early 2025, the specter of catastrophic weather conditions, economic uncertainty, and emerging risks mean caution is warranted for every business as the year unfolds.

Written by

Staff Writer

|April 3, 2025

Jump to section

01

PREMIUM PRICE CHANGES – BY SIZE

02

PREMIUM PRICE CHANGES – BY LINE

03

NOTEWORTHY LINES