Business insuranceInsightsRisk Management

Focus Report – 2025 Food & Agriculture Market Outlook

Written by: Staff Writer | August 13, 2025

Jump to section

01

Recovery, Rebound, and Resilience in the Food and Agriculture Sector

02

Insurance Trends

03

Major Current Challenges

04

Food/Ag Industry Sustainability

05

Emphasis on Resilience

Recovery, Rebound, and Resilience in the Food and Agriculture Sector

The top challenges facing food and agriculture businesses include weather, qualified labor, trucking risks, disease/pests, supply chains, and product liability and recalls. The sector is grappling with margin pressures and changing consumer sentiments, and companies are seeking affordable, innovative ways to control risk and increase profits. Debt in the sector is high, and the number of farms is shrinking. Still, domestic production exceeds consumption, and food and agriculture appear pretty resilient. But there are underlying risks that must be dealt with for the industry to remain strong.

The top challenges facing food and agriculture businesses include weather, qualified labor, trucking risks, disease/pests, supply chains, and product liability and recalls. The sector is grappling with margin pressures and changing consumer sentiments, and companies are seeking affordable, innovative ways to control risk and increase profits. Debt in the sector is high, and the number of farms is shrinking. Still, domestic production exceeds consumption, and food and agriculture appear pretty resilient. But there are underlying risks that must be dealt with for the industry to remain strong.

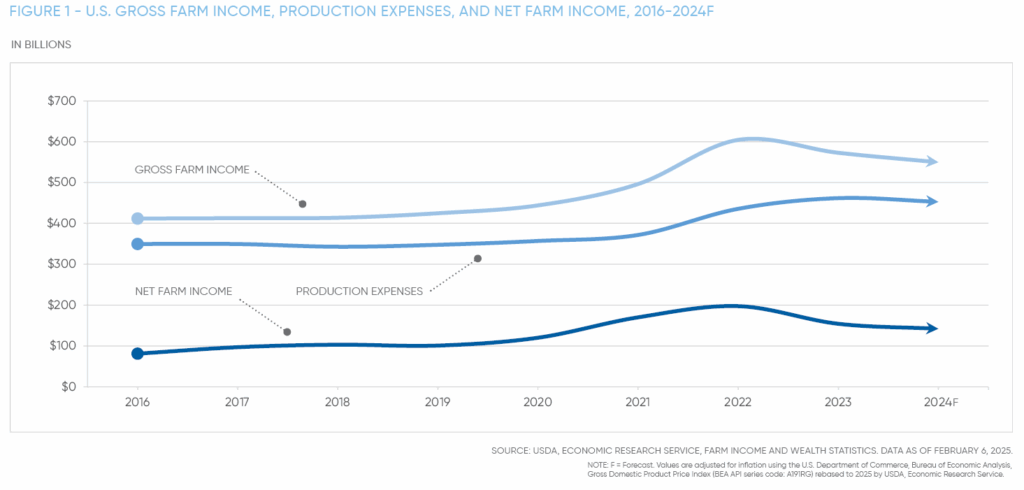

While gross cash farm receipts are expected to rise by 2.9% in 2025, that is largely due to government direct farm program payments. Crop, animal, and animal product cash receipts are all projected to be lower, with farm-related cash income remaining fairly steady, according to the U.S. Department of Agriculture data. Overall net farm income is expected to improve by 26.4% in 2025 after a 7.8% decrease last year. The increase is partially due to a $9 billion decrease in farm production expenses in 2024 and a projected further 2.9% decrease this year, USDA’s Economic Research Service says in its March 12 Farming and Farm Income report.

That said, market volatility continues, and all food and agriculture subsectors are seeking ways to solidify their sustainability and reduce the risk to their assets. The two most prominent perils are natural catastrophes and liability.

Insurance Trends

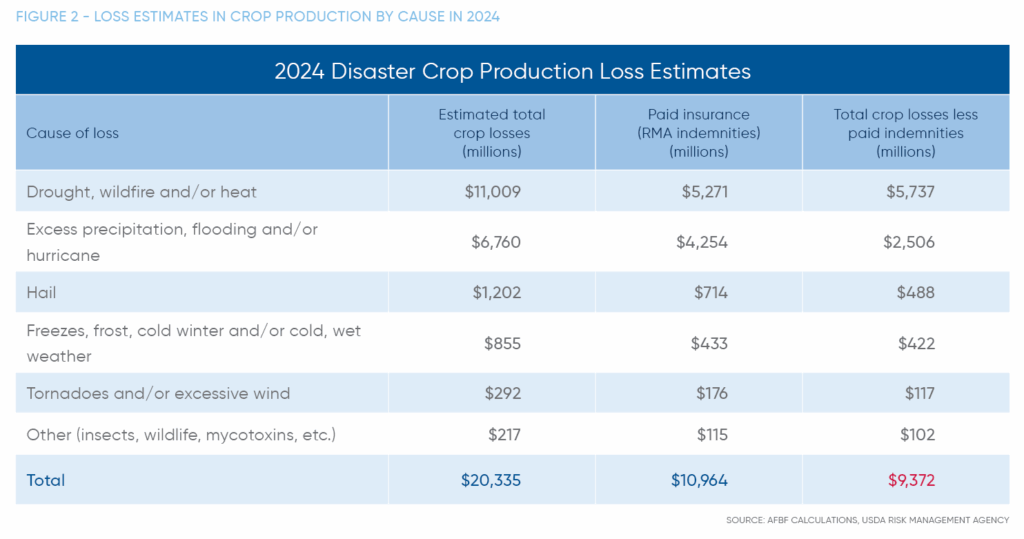

Despite major catastrophes in the United States and worldwide, commercial property insurance premiums increased only 2.9% across the board in the first quarter of 2025, according to the Council of Insurance Agents & Brokers’ (CIAB) Q1 Market Index 2025. Total crop and rangeland losses in 2024 caused by weather catastrophes exceeded $20.3 billion, according to data from the National Oceanic and Atmospheric Administration. Crop insurance was crucial in compensating producers for their losses, with 53% of weather-related damages covered.

The primary food/ag insurance lines experiencing substantial rate increases are commercial auto and product liability, both of which are susceptible to high-damages verdicts.

Some of the largest recent punitive damages in liability lawsuits have been against food and beverage companies. For example, in February 2024, a Nevada jury awarded plaintiffs nearly $130 million in damages for liver injuries suffered after they drank tainted bottled water, $100 million of which were punitive. The same company was hit again with a $5.2 billion award in October, $5 billion of which was punitive.

Additionally, innovative legal theories are generating new food/ag liability lawsuits. For example, a class action complaint is currently seeking plaintiffs who allege ultra-processed food has damaged their organs as well as their financial and mental health. And in April, a judge allowed a nationwide lawsuit against baby food companies to go forward. The plaintiffs allege heavy metals in the food caused brain and neurological damage to babies who ate it.

It’s crucial growers, producers, processors, and sellers have adequate liability insurance limits.

Major Current Challenges

Product liability and tracing, commercial trucking, disease, labor, and market perturbations make for a risk-rich environment in the food and agriculture industry at this point in time.

Product liability and tracing, commercial trucking, disease, labor, and market perturbations make for a risk-rich environment in the food and agriculture industry at this point in time.

Product Liability and Tracing

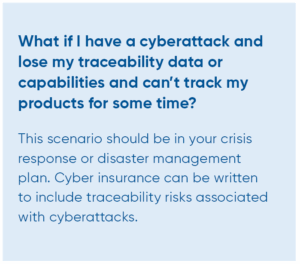

We talked about food traceability last year, and the urgency to adopt top-tier standards remains. Although the Food and Drug Administration announced in March its intention to extend the compliance date for the Food Traceability Rule from January 2026 to June 2028, tracking production and handling is key to protecting those who grow, manufacture, process, pack, or hold food that appears on the Food Traceability List. Having reliable records, even before mandated compliance, will help in a product recall or a product liability claim. It also demonstrates to insurance companies that your business is serious about risk management.

Commercial Trucking

Many food/ag companies rely heavily on commercial trucking to move their product through the distribution pipeline. Some own their own fleets, while others sub out that duty. In either case, moving product is rife with risk—from liability for accident injuries to loss of cargo caused by crashes, theft, vandalism, and spoilage.

Commercial auto insurance has had the highest increases of any sector over the past several years, experiencing a 10.4% increase in the first quarter of 2025, according to CIAB data. This is largely due to high liability verdicts, also known as nuclear verdicts, involving trucking accidents.

Some current challenges we see with auto exposure include lack of quality drivers, driver distraction and/or impairment, and failure to keep vehicles compliant with maintenance and safety standards. When present, these certainly contribute to the rise of high verdicts, often exceeding $10 million. Food and ag risks can take direct action to overcome these challenges by implementing proper driving and employee hiring practices, telematics, cameras, driver monitoring, and detailed vehicle maintenance programs. These actions are no longer nice to have; they are imperative in prevention and loss defense.

Commercial auto and trucking is also a source of product loss. Cargo theft of food and beverage commodities is still rising, with a 242% increase in meat product theft from 2024 to 2025, a 65% increase in alcoholic beverage theft, and a 94% increase in non-alcoholic beverage theft, according to CargoNet. Full truckload thefts are also up, with a 39% increase in semi-trailer heists. Food and beverage producers should insist upon proper theft-prevention measures by trucking contractors or their own drivers and secure appropriate cargo insurance.

Labor Availability

Food production is a highly specialized industry, and laborers typically are highly trained in their niches. Whether workers handle dangerous tools, equipment, or chemicals or are experts at harvesting, packaging, or computerized operations, each brings a valuable skill that is not easily replaceable. Proper employment practices—from hiring to housing to safety on the job—go a long way in protecting food/ag employers from worker and regulator complaints.

Hiring temporary foreign workers is standard practice in the agricultural sector. There is a system in place that works well for businesses that use immigrant labor, and IOA clients get expert assistance with H-2A employment and insurance/safety protections as well as access to exclusive workers compensation markets. Sidestepping the rules, however, can lead to costly government intervention as well as loss of employees and related operational interruptions.

It’s important to assiduously follow labor laws. Regulators are tough on violators. For example, two meat processing companies—one in Maryland and one in Colorado—agreed to pay $4 million each for breaking child labor laws. Contractors to food processing plants have also been fined for supplying youth labor. Investigate Midwest compiled Department of Labor data and says that, over the past two decades, crop production accounts for 49% of all child labor violations that have received a fine by the U.S. Occupational Safety and Health Administration and meatpacking companies comprise 13%.

While the agricultural sector is still one of the worst for worker injuries, there is some good news on the safety front. In food manufacturing, the injury rate dropped to 3.6 cases per 100 full-time workers in 2023, from 4.6 in 2022, according to the U.S. Bureau of Labor Statistics. That still exceeds the 2.7 cases per 100 full-timers across all industries, but it is accompanied by pockets of substantial improvement, such as poultry processing injuries and illnesses, which fell to 2.6 per 100, an 89% decrease from 1994. The agricultural sector’s high numbers for injury and illness underline the need for operational safety and workers compensation insurance. While not all states require workers compensation insurance for farm workers, it’s best to talk with your insurance broker to ensure you understand the insurance requirements in your locale.

Tariffs and Trade

The blockbuster tariffs imposed at the beginning of 2025 have been in flux, with some reductions negotiated and some pauses being granted while talks proceed. Projections for economic potholes abound, but one of the most concerning fears is that foreign farms will gobble up U.S. export market share if countries impose retaliatory tariffs on U.S. agricultural products. Tariffs, however, may have less of an impact on small and midsize farms, which tend to focus sales domestically.

For food and ag companies that do a lot of export business, it may be wise to consider farm revenue protection coverage as part of your crop insurance program. Remember, good historical records on production and revenue are necessary to secure such insurance.

Food/Ag Industry Sustainability

There are four basic measures farms and food/beverage producers can take to improve their ability to survive and thrive:

- Identify and prepare for challenges and interruptions

- Take loss control actions

- Even out losses, cash flow, and costs over time

- Transfer some risk to an insurance program

Weather is probably the biggest threat to the food/ag industry that can’t be changed in terms of frequency or severity of the event. But farms and food/beverage companies can be prepared for natural disasters by having the proper insurance and amount of coverage and by establishing and practicing a catastrophe response plan. Some response plans include protective measures for property and equipment as well as backup energy sources for irrigation, temperature controls, automated processes, building/room access, etc.

Natural disasters don’t affect just your property, so plans for alternative suppliers and distributors should be included in case primary companies are damaged, destroyed, blocked, or delayed.

There are other problems that affect the supply chain as well. These include political perils such as blockades, war, and strikes/civil commotion. Being prepared with supply chain insurance may help you with losses associated with many of these incidents.

Since trucking is a top loss exposure, truck drivers should be fully vetted before hiring, with driving history, drug testing, and valid CDL verification as priorities. They also should be monitored for rules compliance while behind the wheel. While unpopular with drivers, telematics, in-cabin cameras, and dashcams are all very helpful when it comes to making sure drivers are following safety rules. They also can supply evidence in erroneous, overstated, or fraudulent liability claims and cases of theft.

Since trucking is a top loss exposure, truck drivers should be fully vetted before hiring, with driving history, drug testing, and valid CDL verification as priorities. They also should be monitored for rules compliance while behind the wheel. While unpopular with drivers, telematics, in-cabin cameras, and dashcams are all very helpful when it comes to making sure drivers are following safety rules. They also can supply evidence in erroneous, overstated, or fraudulent liability claims and cases of theft.

Superior loss control also encompasses good training programs for all workers and helping new hires develop expertise where they need it. Having online learning modules can complement on-the-job training for safety, proper use of equipment, and proper biomechanics. Managers should ensure application of lessons learned. An effective way to ensure safety is for each manager to check and secure all protective equipment and cover recent types of incidents or near-misses prior to each shift with their group to help keep the same type of injury from occurring again.

With bottom-line protection a prized outcome in this tight-margin industry, evening out losses, cash flow, and costs over time is often a goal. Since some years are booms and some are busts, it may be smart to have storage plans (and insurance to cover stored product), forward contracting, and agreements with alternative suppliers.

Since the cost of capital is a pressing concern in this high farm-debt environment, commodities companies are looking for creative financing solutions. This is especially true for those facing significant capital requirements from exchanges and futures clearing merchants and those heavily dependent on imports. While the financial mechanisms are complicated, one thing is clear: insurance on crops, cargo, and supply chains should correspond to the requirements of these commodity finance contracts. Gaps here can lead to substantial transactional risk exposures.

Insurance is a key way to keep your bottom line on an even keel. Not only is insurance geared to help balance losses and expenditures over time, it also can be structured with respect to your cash flow needs. For example, workers compensation can be structured as a monthly, pay-as-you-go plan to reflect seasonal ebbs and flows in employee levels. Risk transfer and insurance coverage in areas such as cyber, product recall, or crop insurance can be underutilized but provide necessary solutions to real exposures felt by food and ag risks. With a 28% increase in USDA food product recalls in 2024, according to Sedwick’s Q1 2025 Recall Index, all companies in the food and agricultural sector should consider the full array of insurance options. We know that smaller producers especially are generally underinsured.

Crop insurance can provide additional bottom line solutions to even out cash flow needs for farmers and growers. It is estimated that, in 2022, some 62% of row crop farms purchased crop insurance from the federal program along with only 9% of those growing specialty crops, such as fruits, vegetables and nursery crops, according to the USDA’s America’s Farms and Ranches at a Glance: 2023 Edition. Insurance protection for many crops can be available but significantly underutilized. Crop insurance can help combat pressures compounded by climate volatility. By providing a crucial safety net, revenue protection, and peace of mind, crop insurance enables growers to recover from catastrophic events. This is why IOA has a close partnership with Agrilliance, one of the nation’s largest and most experienced crop insurance agencies.

Crop insurance can provide additional bottom line solutions to even out cash flow needs for farmers and growers. It is estimated that, in 2022, some 62% of row crop farms purchased crop insurance from the federal program along with only 9% of those growing specialty crops, such as fruits, vegetables and nursery crops, according to the USDA’s America’s Farms and Ranches at a Glance: 2023 Edition. Insurance protection for many crops can be available but significantly underutilized. Crop insurance can help combat pressures compounded by climate volatility. By providing a crucial safety net, revenue protection, and peace of mind, crop insurance enables growers to recover from catastrophic events. This is why IOA has a close partnership with Agrilliance, one of the nation’s largest and most experienced crop insurance agencies.

Emphasis on Resilience

Using any or all of these methods, food and agricultural businesses can thrive even in the uncertain market conditions of today.

And with risk transfer experts, loss control specialists, special market access, and advisory services, IOA helps food and agribusiness clients recover from damage, strengthen their company, and protect their bottom line.

To request a copy of the full report, email marketing@ioausa.com.

Written by

Staff Writer

|August 13, 2025

Jump to section

01

Recovery, Rebound, and Resilience in the Food and Agriculture Sector

02

Insurance Trends

03

Major Current Challenges

04

Food/Ag Industry Sustainability

05

Emphasis on Resilience