Business insuranceInsightsRisk Management

Market Softening Accelerates as Competition Intensifies

Written by: Bevrlee Lips | January 30, 2026

Jump to section

01

PREMIUM PRICE CHANGES – BY SIZE

02

PREMIUM PRICE CHANGES – BY LINE

03

NOTEWORTHY LINES

04

OUTLOOK

An overview of The Council of Insurance Agents & Brokers’ Commercial Property/Casualty Market Index Q3/2025 and marketing conditions ahead

Each quarter, The Council of Insurance Agents & Brokers releases its Commercial Property/Casualty Market Index. Here, we review the Q3 2025 findings, which utilize data from July 1 through September 30, 2025. We also consider current conditions to provide context for risk transfer solutions and strategic planning for emerging risks.

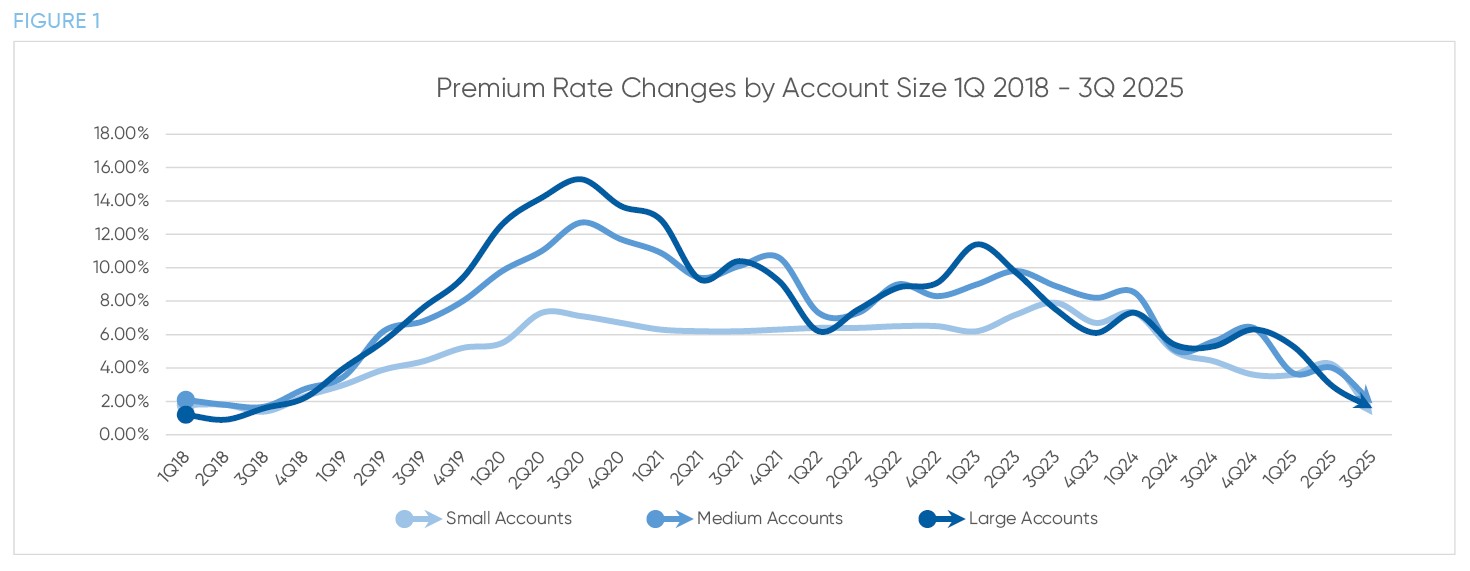

PREMIUM PRICE CHANGES – BY SIZE

The commercial insurance market showed unmistakable soft market conditions in Q3 2025, with average premium increases across all account sizes easing to just 1.6%, down from 3.7% in Q2. This marked the 32nd consecutive quarter of average premium increases, but the magnitude of increases has declined to levels not seen since two years before the pandemic period.

Small accounts led the moderation with premium increases of just 1.2%, down considerably from 4.2% in Q2. Multiple respondents highlighted aggressive carrier competition for small business, with one Northwestern firm noting that carriers have been particularly interested in smaller accounts. Medium accounts saw increases of 1.9%, a welcome decrease from the previous quarter’s 4.0%, while large accounts experienced a 1.6% increase, down from 2.9% in Q2.

Several index respondents commented that carriers were markedly more competitive and even aggressive in their pursuit of new business, which was likely a key driver behind the notable moderation in this quarter’s rate increases.

PREMIUM PRICE CHANGES – BY LINE

Q3 2025 demonstrated clear soft market conditions across the board. All lines of business showed premiums that were either flat or lower compared to Q2, with no exceptions this quarter. The number of lines recording actual premium decreases rose from five to six: business interruption (-0.2%), commercial property (-0.2%), cyber (-2.6%), D&O (-2.1%), employment practices (-0.7%), and workers compensation (-1.9%).

Across the five major lines of business—commercial auto, commercial property, general liability, umbrella, and workers compensation—average premiums increased by just 2.7%, a 45% decrease from the previous quarter’s 4.9%. As one respondent from a large Northeastern firm observed, “We are in a stable to soft market for most lines.”

NOTEWORTHY LINES

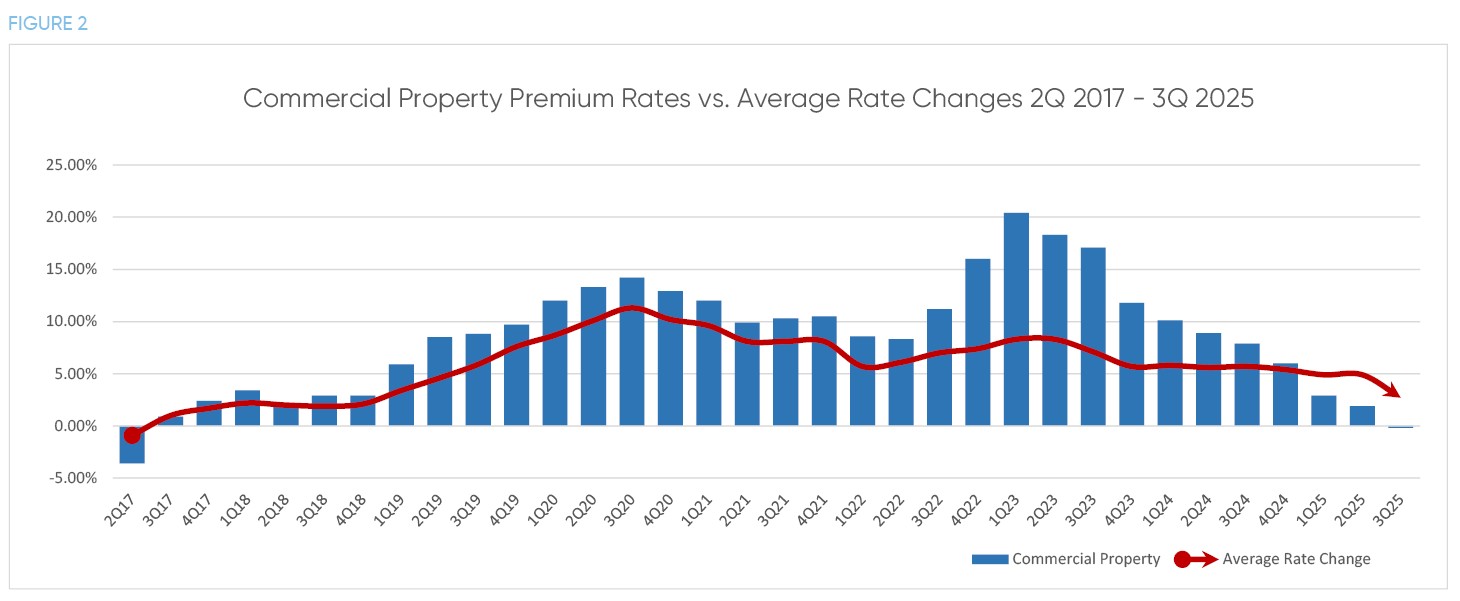

Commercial Property

Commercial Property

Commercial property premiums decreased by 0.2% in Q3, marking the first decline in property premiums since Q2 2017. This was a dramatic shift from peak premium increases of 20.4% in Q1 2023.

More than half of survey respondents reported an increase in underwriting capacity. Industry sources pointed to a wave of new carriers and MGAs entering the property market, along with some carriers reentering after exiting in 2023.

Additionally, the commercial property reinsurance market has softened considerably, allowing primary property carriers to reduce costs and pass savings on to insureds.

However, IOA has cautioned in previous reports that client rates will vary depending on sector and region. As Amwins noted in its State of the Market – 2026 Outlook, “Some sectors are experiencing favorable rate movement and improved underwriting results, while others still face tougher challenges.” This is where an expert advisor with a keen understanding of your business and deep carrier relationships makes a significant difference.

Carriers in the commercial lines space may feel they have reached adequate premiums on most accounts, noted the AM Best 2025 Market Segment Report, which also pointed to “an improvement in the commercial property reinsurance market, allowing primary property carriers to reduce costs.”

Competition within the property space increased meaningfully throughout 2024, and that trend continued into 2025, noted Amwins in its April 2025 property update. The report also stated, “Common sentiment is that this is one of the most rapid erosions of property market conditions in decades.” This has remained true in the months that have followed.

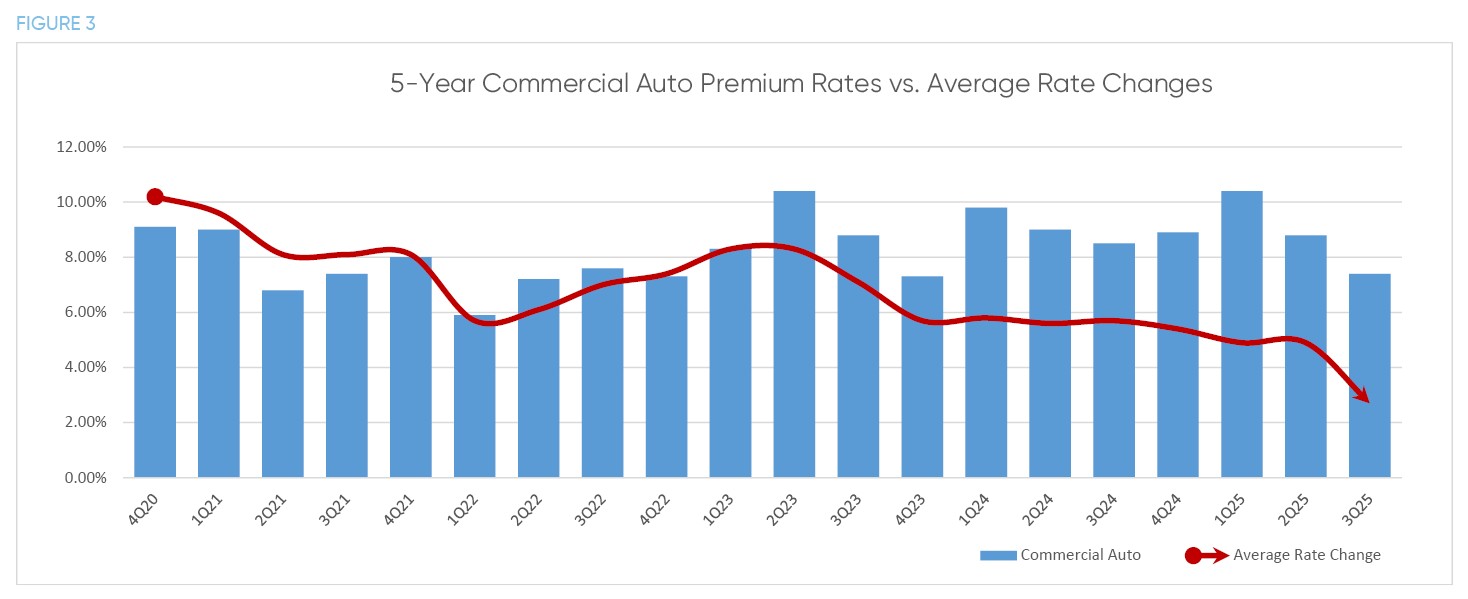

Commercial Auto

Commercial Auto

Commercial auto remained the most challenged line, with premiums increasing by 7.4% in Q3, though this represented a continued deceleration from 8.8% in Q2 and 10.4% in Q1. The line continues to be impacted by rising claim severity and frequency, though the downward trend in rate increases suggests some stabilization may be emerging.

Smart risk management tools and controls that monitor driver behavior and aid in accident prevention remain essential for keeping losses down and securing favorable terms and pricing.

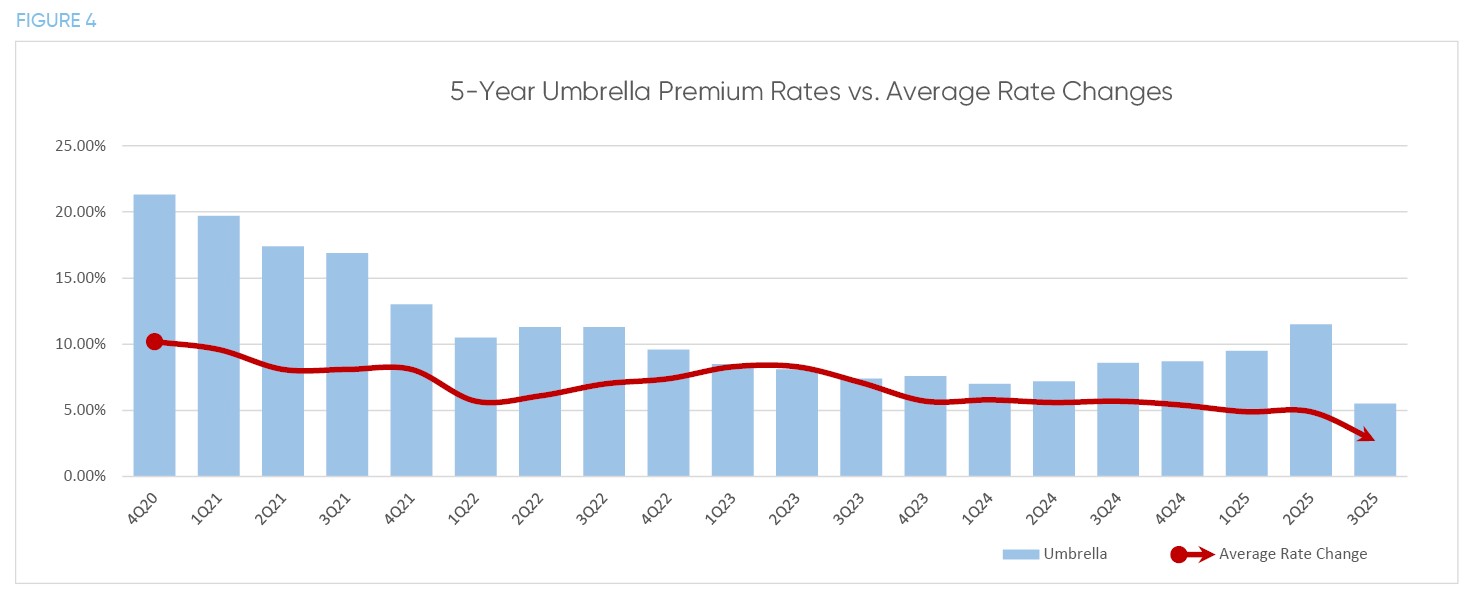

Umbrella

Umbrella

Umbrella coverage showed a surprising reversal, with premiums rising by just 5.5% in Q3 compared to 11.5% in Q2. This dramatic 52% decrease in the rate of increase represents an abrupt shift for a line that had been steadily climbing since Q1 2024. Corroborating this trend is third-party data from Ivans, which also reported a deceleration in umbrella rate increases. CIAB noted that it is “not yet clear what may be influencing this abrupt reversal in the magnitude of average premium increases for the line.”

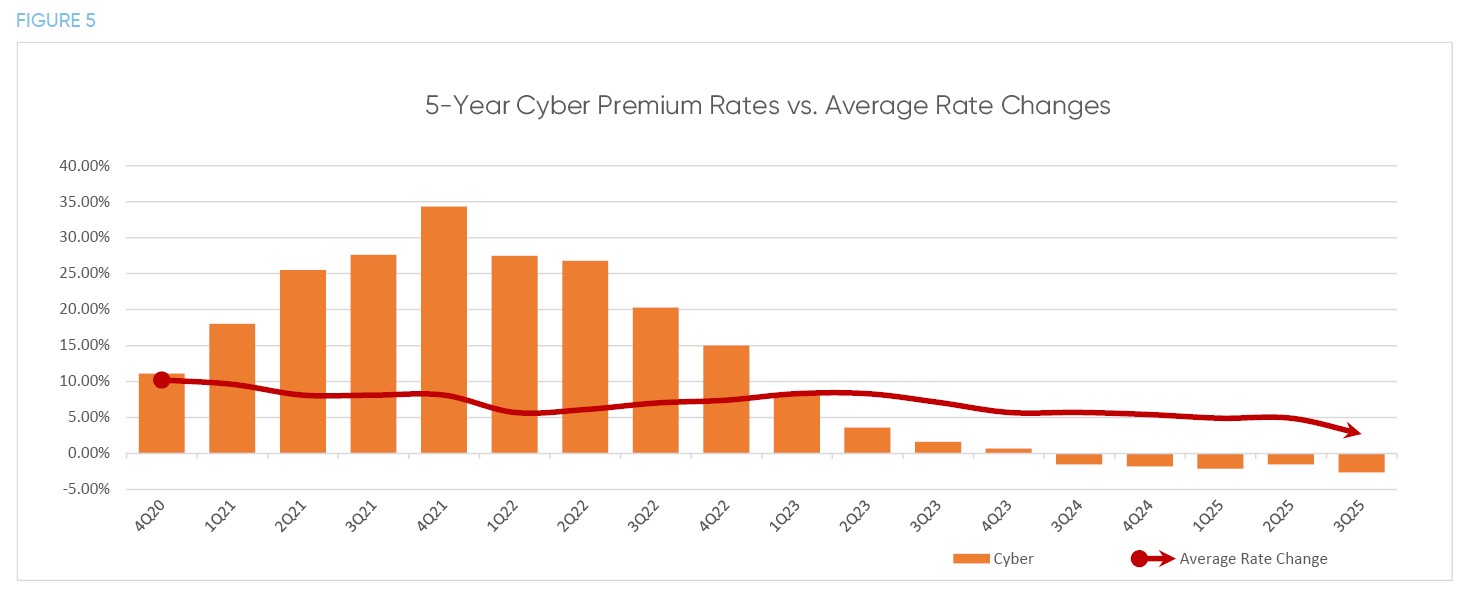

Cyber

Cyber

Cyber premiums saw another record-setting decrease and the largest of any line, falling an average of 2.6% in Q3, the fourth record decrease set by the line in the past six quarters. This soft market is being driven by abundant capacity and fierce competition among carriers.

An increase in cyber underwriting capacity was reported by 43% of respondents, with a quarter of them characterizing the increase as significant. The main sources of capital include a favorable reinsurance market and recent growth in the cyber insurance-linked securities (ILS) bond market. In 2024 alone, the cyber-ILS market deployed over $750 million in 144A cyber cat bonds.

Survey respondents saw a 45% increase in demand, which attracted more than enough carriers to the line. This supply/demand imbalance has created a buyer’s market, with lower premiums and more favorable terms for organizations that demonstrate strong cybersecurity practices.

An emerging risk for the line includes artificial intelligence (AI), which policy language in many cases does not adequately address. Make sure to address this and other emerging and ongoing risks with your insurance advisor.

OUTLOOK

Data confirms that the commercial insurance market has entered a definitively soft phase for most lines. The dramatic deceleration in premium increases across all account sizes and the growing number of lines experiencing actual premium decreases point to a highly competitive marketplace.

Business owners should leverage current market conditions to secure favorable terms and focus on strong risk management practices to maintain their competitive positioning, as market cycles inevitably will shift.

Written by

Bevrlee Lips

|January 30, 2026

Jump to section

01

PREMIUM PRICE CHANGES – BY SIZE

02

PREMIUM PRICE CHANGES – BY LINE

03

NOTEWORTHY LINES

04

OUTLOOK