Business insuranceInsightsRisk Management

Market Stability Strengthens as Verdicts Continue to Go Thermonuclear

Written by: Bevrlee Lips | September 30, 2025

Jump to section

01

PREMIUM PRICE CHANGES – BY SIZE

02

PREMIUM PRICE CHANGES – BY LINE

03

NOTEWORTHY LINES

04

LITIGATION TRENDS AND LEGISLATIVE RESPONSE

05

OUTLOOK

An overview of The Council of Insurance Agents & Brokers’ Commercial Property/Casualty Market Index Q2/2025 and marketing conditions ahead

Each quarter, The Council of Insurance Agents & Brokers releases its Commercial Property/Casualty Market Index. Here, we review the Q2 2025 findings, which utilize data from April 1 through June 30, 2025. We also consider current conditions to provide context for risk transfer solutions and strategic planning for emerging risks.

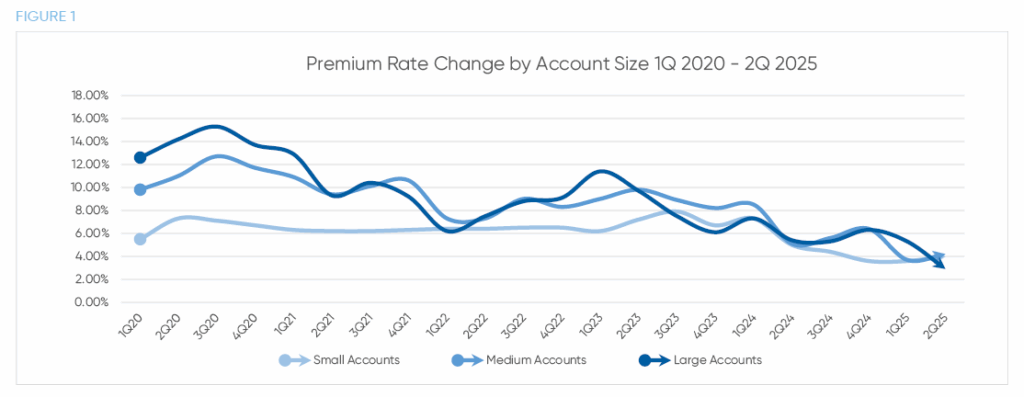

PREMIUM PRICE CHANGES – BY SIZE

The commercial insurance market saw continued softening in Q2 2025 with average premium increases coming in at 3.7% across all account sizes, down from 4.2% in Q1. This marked the 31st consecutive quarter of premium growth, but the pace has decelerated considerably since the double-digit highs of 2020.

Premium increases varied by account size with large accounts seeing the most dramatic shift. Rates for large accounts rose by just 2.9% in Q2, a sharp decline from 5.3% in Q1. Respondents expressed uncertainty about factors that contributed to the change. While some noted more aggressive carrier pursuit accompanied by additional capacity, others pointed to the persistence of upward pressure. Medium accounts experienced a 4.0% increase, while small accounts saw a slightly higher average increase of 4.2%, compared to 3.7% and 3.6% respectively in the previous quarter.

PREMIUM PRICE CHANGES – BY LINE

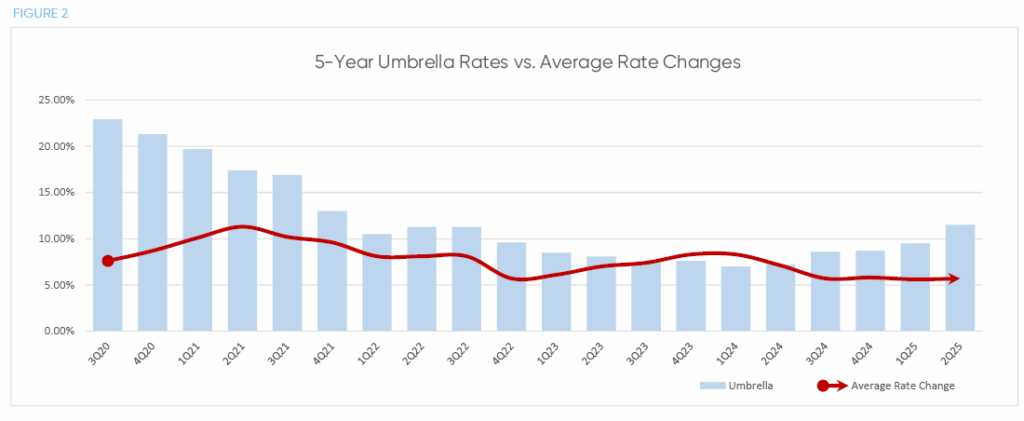

Premium increases moderated across most lines of business compared to the previous quarter, coming in flat or slightly lower than in Q1. For the five major lines of business—commercial auto, commercial property, general liability, umbrella, and workers compensation—average overall rates remained steady at 4.9%. Of that group, however, umbrella rose 11.5%, offsetting slight increases and decreases in other lines.

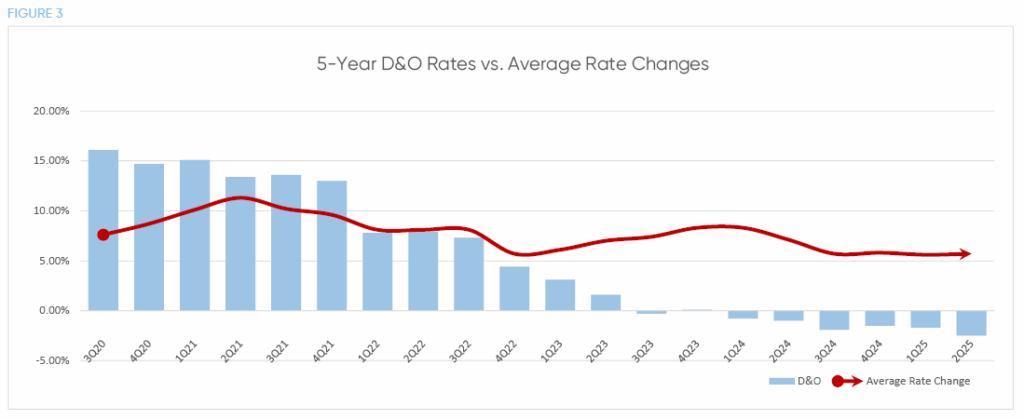

For the second time, five lines recorded actual decreases—cyber, D&O, employment practices, terrorism, and workers compensation.

NOTEWORTHY LINES

Umbrella

Umbrella coverage continues to be the most challenged line, with premiums rising by 11.5% in Q2. This increase was driven largely by the surge in litigation severity, including a record number of nuclear verdicts exceeding $10 million and thermonuclear verdicts surpassing $100 million. Some carriers are responding by tightening underwriting criteria and reducing available limits—often offering $2 million to $5 million layers compared to the previous standard of $10 million. This has necessitated more complex layering to reach desired limits.

Umbrella coverage continues to be the most challenged line, with premiums rising by 11.5% in Q2. This increase was driven largely by the surge in litigation severity, including a record number of nuclear verdicts exceeding $10 million and thermonuclear verdicts surpassing $100 million. Some carriers are responding by tightening underwriting criteria and reducing available limits—often offering $2 million to $5 million layers compared to the previous standard of $10 million. This has necessitated more complex layering to reach desired limits.

D&O

D&O liability saw the largest decline among all lines, with premiums dropping by 2.5%, followed closely behind by employment practices at -1.8%. For the balance of 2025, challenges for D&O include macroeconomic uncertainty, such as tariff impacts, social inflation, third-party litigation funding as well as cybersecurity risks and disclosures to name a few, according to AM Best Senior Industry Research Analyst Christopher Graham.

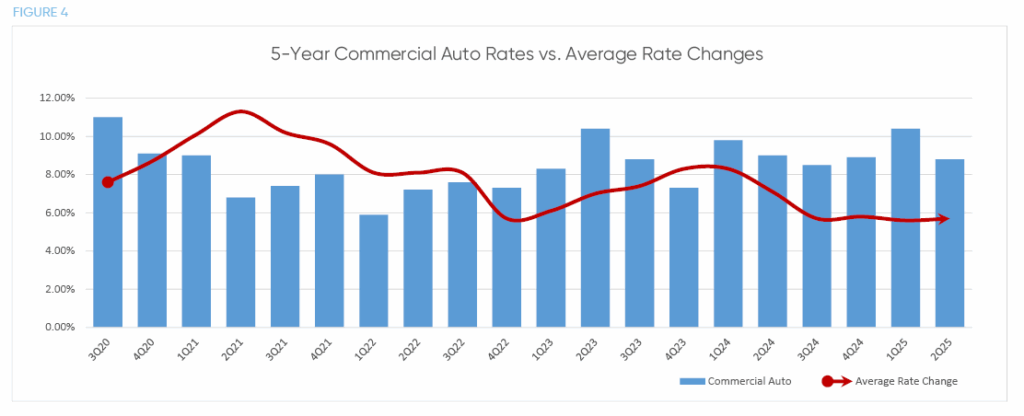

Commercial Auto

Commercial auto also remains under pressure, with premiums increasing by 8.8%. While slightly down from 10.4% in Q1, the line continues to be impacted by rising claim severity and frequency. Smart risk management tools and controls, such as those that monitor driver health and behavior and aid in accident prevention, can help in keeping losses down and securing favorable terms and pricing.

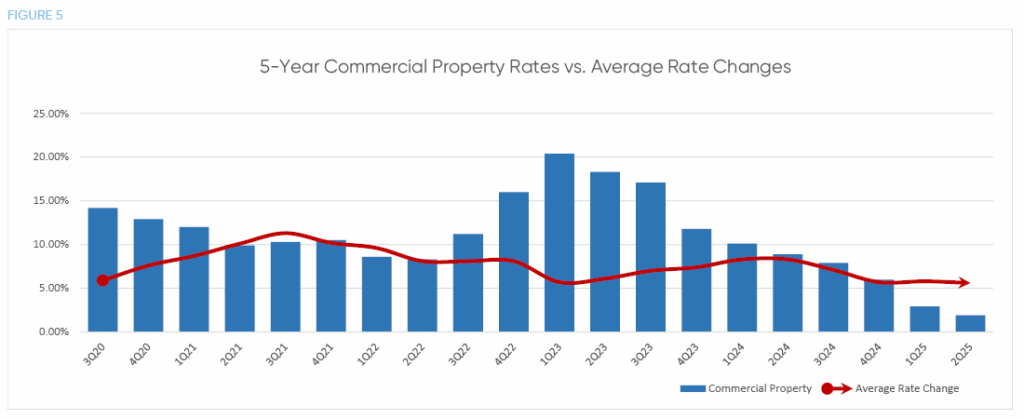

Commercial Property

Coming in at a low 1.9% increase, commercial property rate increases have seen a nearly 70% deceleration since the end of 2024. While this is good news at the macro level, rates at the micro level have become increasingly influenced by both regional factors and individual property characteristics. Having a broker with extensive carrier relationships will be essential for property owners navigating complex coverage options.

Looking ahead, rates are expected to be shaped by five main factors: natural disaster frequency, reinsurance capacity, underinsurance concerns, labor shortages, and replacements costs.

Workers Compensation

Workers compensation remained in decline, with premiums falling by 1.8%, continuing a multiquarter trend of softening due to strong loss ratios and competitive market conditions. Respondents noted that workers compensation and D&O provided an avenue to offset lines with higher increases, such as umbrella.

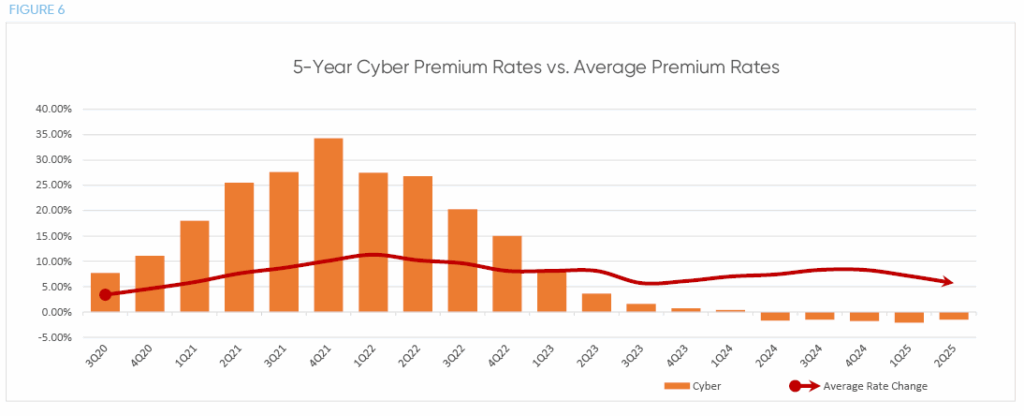

Cyber

Cyber liability softened slightly with a 1.5% decrease as improved risk controls and market maturity continue their stabilizing affect on pricing. Swiss Re Group noted in its September 2025 update that, “Increased market competition is a key reason why cyber is now in its third consecutive year of rate reductions, as cyber insurance supply continues to outstrip demand.” However, “the cyber threat landscape and loss trend environment are continuing to evolve rapidly.” Caution is warranted as systemic loss events and rising privacy liability litigation take place in a market still seeking sustainable stabilization.

LITIGATION TRENDS AND LEGISLATIVE RESPONSE

The litigation environment increasingly is influencing underwriting decisions, particularly in umbrella and auto liability. In 2024, there were 135 nuclear verdicts and 49 thermonuclear verdicts, many of which were concentrated in product liability, auto, and intellectual property cases, according to Marathon Strategies data. The accompanying rise of third-party litigation funding (TPLF) has further complicated the landscape, prompting carriers to reassess their exposure and reduce limits.

In Triple-I/Munich Re US’s report A Consumer Guide: How Legal System Abuse Impacts You, the devastating result of legal system abuse is made apparent:

- $6,664 in added annual costs for the average American family of four

- 4.8 million jobs lost in the U.S. economy due to excessive litigation

- Over $160 billion in annual tort costs for small businesses

At the federal level, Rep. Darrell Issa, R-Calif., chairman of the House Subcommittee on Courts, Intellectual Property, Artificial Intelligence, introduced in February the Litigation Transparency Act of 2025 (HR 1109), which would require disclosure of TPLF in federal civil cases, and the Protecting Our Courts from Foreign Manipulation Act of 2025 (HR 2675) was introduced in April by Rep. Ben Cline, R-Va. The number of states introducing

OUTLOOK

IOA expects the softening trend to continue between now and the end of the year, particularly in lines with favorable loss experience and abundant capacity. However, litigation risks will remain a key factor shaping carrier strategies and pricing decisions as will the ever-unpredictable impact of natural catastrophe events.

IOA remains committed to helping clients navigate this dynamic market with clarity, strategy, and confidence.

Written by

Bevrlee Lips

|September 30, 2025

Jump to section

01

PREMIUM PRICE CHANGES – BY SIZE

02

PREMIUM PRICE CHANGES – BY LINE

03

NOTEWORTHY LINES

04

LITIGATION TRENDS AND LEGISLATIVE RESPONSE

05

OUTLOOK