Business insuranceInsightsRisk Management

Softening Market Conditions Continue as Litigation Front Amps Up

Written by: Staff Writer | June 23, 2025

Jump to section

01

PREMIUM PRICE CHANGES – BY SIZE

02

PREMIUM PRICE CHANGES – BY LINE

03

NOTEWORTHY LINES

04

OUTLOOK

An overview of The Council of Insurance Agents & Brokers’ Commercial Property/Casualty Market Index Q1/2025 and marketing conditions ahead.

Each quarter, The Council of Insurance Agents & Brokers releases its Commercial Property/Casualty Market Index. Here, we review the Q1 2025 findings, which utilize data from January 1 through March 31, 2025. We also consider current conditions to provide context for risk transfer solutions and strategic planning for emerging risks.

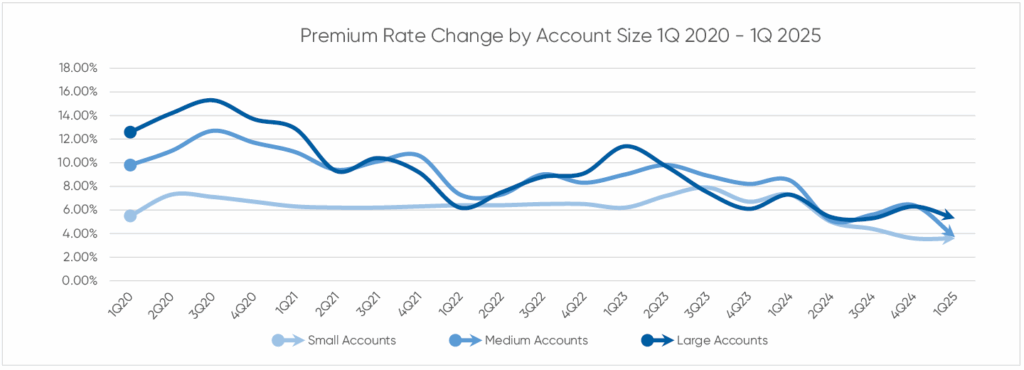

PREMIUM PRICE CHANGES – BY SIZE

The commercial lines market continued its transition toward more stable conditions in Q1 2025, with average premium increases across all account sizes dropping to 4.2%, down significantly from 5.4% in Q4 2024. This continues the moderation trend we’ve observed in recent quarters, suggesting a potential shift toward a softer market. However, it was the 30th consecutive quarter in which premium increases were seen across all account sizes.

The commercial lines market continued its transition toward more stable conditions in Q1 2025, with average premium increases across all account sizes dropping to 4.2%, down significantly from 5.4% in Q4 2024. This continues the moderation trend we’ve observed in recent quarters, suggesting a potential shift toward a softer market. However, it was the 30th consecutive quarter in which premium increases were seen across all account sizes.

Medium accounts experienced the most dramatic change with premium increases slowing to 3.7%, nearly half that of the previous quarter at 6.4%. Small accounts maintained steady premium increases at 3.6%, and large accounts also saw a cooling coming in at 5.3%, down from 6.3%.

PREMIUM PRICE CHANGES – BY LINE

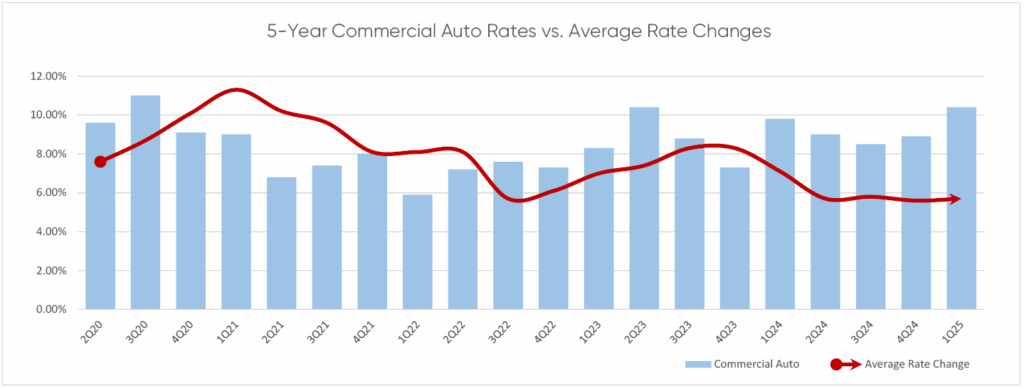

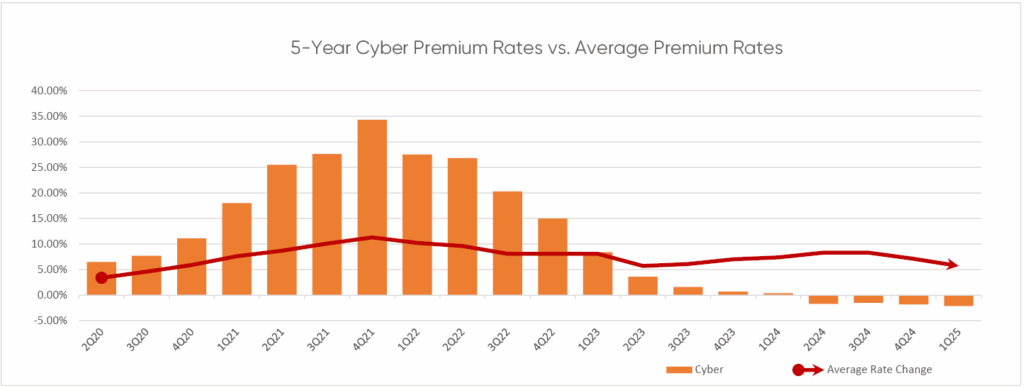

Reported average premium increases were lower for all but two lines—commercial auto and umbrella—compared to Q4 2024. A growing number of lines showed premium decreases with five lines reporting negative growth: cyber (-2.1%), D&O (-1.7%), employment practices liability (-0.4%), terrorism (-0.4%), and workers compensation (-2.6%).

For the second consecutive quarter, commercial auto experienced the highest premium increase at 10.4%, up from 8.9% in Q4 2024. Umbrella followed closely with a 9.5% increase, up from 8.7% in the previous quarter. These two lines continue to face significant upward pressure due to social inflation, nuclear verdicts, and increased claims severity.

Pressures for this period included “frequency and severity of claims, premium, and even coverage terms and conditions like limits or sublimits.” Third-party litigation funding (TPLF) also is having a profound impact on the insurance industry— particularly verdict sizes for commercial auto and umbrella. In response, there is a groundswell of proposed legislation making its way through at the state and national level.

“Thirty-five separate bills have been introduced in U.S. statehouses so far this year,” said the Insurance Information Institute (III). “The efforts are not only progressing at the state level. The U.S. House of Representatives is advancing HR 1109 – The Litigation Transparency Act of 2025 – which would regulate third-party litigation funding in federal court cases.” Click here for the status of HR 1109.

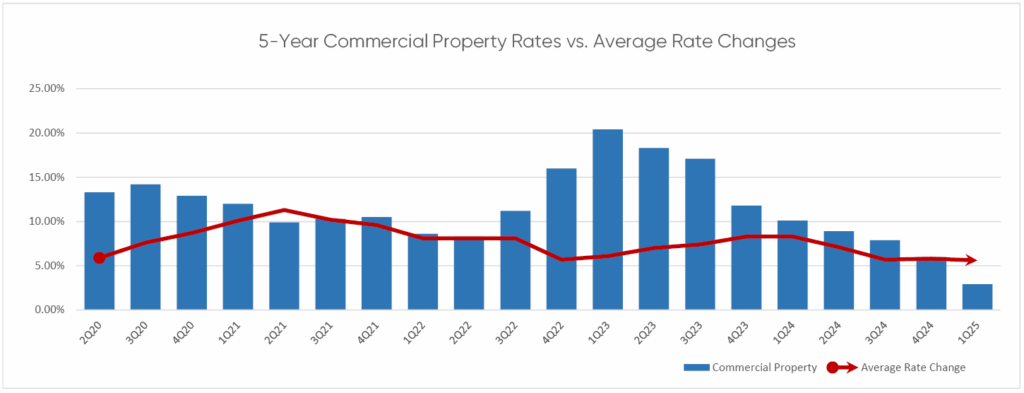

D&O saw increased competition among carriers and there also was perceived additional capacity. General liability premiums increased by 4.2%, while commercial property premiums rose by a modest 2.9%, continuing the downward trend observed throughout 2024.

NOTEWORTHY LINES

Commercial Auto

Commercial Auto

Commercial auto premiums outpaced other lines in Q1 2025 coming in at 10.4%. Cost drivers impacting market conditions remained plentiful for commercial auto, including rising claims severity, higher repair costs due to advanced vehicle technology, limit restrictions, and underwriting capacity constraints, to name a few.

Fleet electrification continues to present challenges as well with the higher initial cost of electric vehicles and specialized repair requirements contributing to premium increases. Additionally, TPLF has been identified as a significant factor in driving up commercial auto claim costs and subsequent premium increases.

Umbrella

Umbrella had the second-highest average increase at 9.5%, which was attributed to continued social inflation, nuclear verdicts, and a “more cautious underwriting posture” from carriers.

Respondents also highlighted the impact of TPLF on umbrella coverage, noting that it has significantly affected both claim amounts and availability of coverage. Higher umbrella limits were not available for certain types of risk due to carriers pulling back in response to TPLF.

Commercial Property

Commercial Property

Commercial property premiums increased by 2.9% in Q1 2025, down significantly from the 6.0% increase observed in Q4 2024. This marks the 8th consecutive quarter of deceleration for commercial property premiums, continuing the trend that began in Q2 2023. Conditions were competitive and increasingly flexible, allowing for better terms at renewal. The line has seen significant change from its 20.4% average increase just two years ago.

Workers Compensation

Workers compensation premiums decreased by 2.6%, continuing the downward trend observed in the previous 12 consecutive quarters. This line continues to be a bright spot in the commercial insurance market, with strong underwriting results and increased carrier competition driving favorable pricing for insureds.

Cyber

Cyber premiums decreased by 2.1%, marking the 4th consecutive quarter of premium decreases for cyber insurance, primarily driven by increased competition among U.S. carriers and expanded underwriting capacity.

Despite the continued prevalence of ransomware attacks, improved risk controls and cyber resilience measures implemented by insureds have contributed to better underwriting results and subsequent premium easing. Carriers continue to reward organizations that demonstrate strong cybersecurity practices with more favorable terms and conditions.

OUTLOOK

While Q1 2025 data shows clear signs of market softening in several lines, certain segments continue to face upward pressure. This market environment presents both opportunities and challenges for insureds, with favorable conditions in some lines offsetting continued hardening in others.

As we move further into 2025, the commercial insurance market appears to be transitioning toward more balanced conditions. While certain lines like commercial auto and umbrella continue to face challenges, the overall trend suggests increasing stability and moderation in premium increases.

Factors that may influence market conditions in the coming quarters include:

- The ongoing impact of third-party litigation funding on claim severity and coverage availability.

- Reinsurance market dynamics, particularly in response to catastrophic events.

- Economic conditions and their effect on claim frequency and severity.

- Technological advancements in risk assessment and underwriting processes.

- Regulatory developments affecting key coverage lines.

Organizations that proactively address these factors through comprehensive risk management strategies will be better positioned to navigate the evolving insurance landscape in 2025.

Written by

Staff Writer

|June 23, 2025

Jump to section

01

PREMIUM PRICE CHANGES – BY SIZE

02

PREMIUM PRICE CHANGES – BY LINE

03

NOTEWORTHY LINES

04

OUTLOOK