Business insuranceInsightsPersonal insuranceRisk Management

The 2025 Hurricane Season Kicks Off with Above-Normal Atlantic Activity Predicted

Written by: Bevrlee Lips | June 1, 2025

Jump to section

01

A Mixed Bag of Predicted Activity

02

Now Is the Time to Review Your Coverage

03

Check the Details of Your Insurance Policy

04

Know Your Hurricane Deductible & Other Costs

05

Update Your Policy to Reflect Your Needs

06

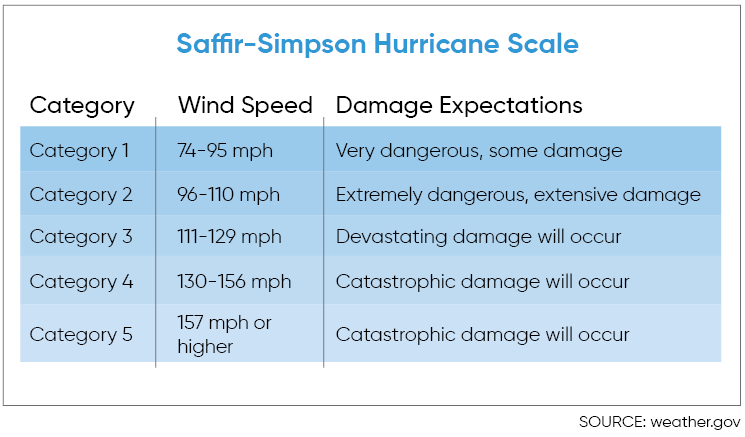

Saffir-Simpson Hurricane Scale

As we head into summer, many property owners in the United States are reminded of one thing: our blissful hiatus is over. It’s hurricane season once again. The Atlantic season begins on June 1 and the Pacific season begins May 15, with both ending November 30. Tropical Storm Alvin kicked things off early on May 29 by becoming the first named storm anywhere in the Northern Hemisphere this year. So what is expected this season and how can you prepare?

A Mixed Bag of Predicted Activity

The National Oceanic and Atmospheric Administration (NOAA) released its predictions for the 2025 season based on several factors, including “warmer than average ocean temperatures, forecasts for weak wind shear, and the potential for higher activity from the West African Monsoon, a primary starting point for Atlantic hurricanes.” ENSO (El Niño-Southern Oscillation) conditions also are considered in the calculations, and they are expected to be neutral in both the eastern Pacific and Atlantic.

“The high activity era continues in the Atlantic Basin, featuring high-heat content in the ocean and reduced trade winds. The higher-heat content provides more energy to fuel storm development, while weaker winds allow the storms to develop without disruption,” according to NOAA.

What does it all mean? The result is a mixed bag of expectations across the regions. An above-normal hurricane season is predicted for the Atlantic region with other regions near or below normal (see chart below).

Now Is the Time to Review Your Coverage

With an overall increase in storms causing at least $1 billion in damages, it’s more important than ever to make sure your assets are protected in the event of a natural disaster.

Unfortunately, many property owners delay purchasing or updating their insurance coverage until a storm is approaching. However, insurance companies often impose a moratorium on issuing new policies or making changes to existing policies once a named storm is projected to impact a region where it provides coverage. That makes now the best time to take action to protect your property and belongings from potential damage.

Check the Details of Your Insurance Policy

In addition to what is provided in a standard homeowners policy, it is important to consider other coverages that essentially amount to hurricane insurance. A combination of these policies can close gaps in the protection of your property.

Windstorm Coverage

If you live in an area that experiences high-wind and hail events, you may want to consider adding windstorm coverage. Most policies will have a percentage deductible, and coverage applies whenever damage is caused by wind, hail, or other named perils. It raises coverage limits and typically goes into effect after 15 days. Perils such as flooding and fire are not covered under this type of policy.

Flood Insurance

It’s a common misconception that flood damage coverage is included in homeowners insurance policies, but that is not the case. Damage resulting from stormwater, an overflowing body of water, or other similar events typically are not covered.

The Federal Emergency Management Agency (FEMA) states that, “Flooding is the most common and costly natural disaster in the United States. In the past five years, all 50 states have experienced floods or flash floods. Even just one inch of water can cause $25,000 of damage to your home.”

If you live in a high-risk area for flooding, you may be required to have flood insurance. If not, it still may be a prudent consideration for your home or property. Keep in mind that flood insurance policies typically go into effect after 30 days, so purchasing this option well in advance of a natural disaster or storm event is crucial.

Comprehensive & Collision Auto Coverage

If you’ve purchased an auto collision policy, you are protected from damage to your vehicle in the event it collides with another vehicle, person, or object, whether you or someone else is at fault. That includes flash flooding, falling trees, or other damages caused by a storm. For damage not caused by a collision, comprehensive coverage provides protection for damage from hurricanes, fire, flood, and other acts of nature. Coverage typically goes into effect upon receipt of payment.

Know Your Hurricane Deductible & Other Costs

In most high-risk states, homeowners insurance policies contain a percentage deductible for hurricane coverage, which typically falls between 1% and 5% of the home’s insured value. For example, if your home is worth $300,000 and you have a 3% hurricane deductible, you’re responsible for paying the first $9,000 in damages before coverage goes into effect. If you’re unaware of what your hurricane deductible is, make sure you check your policy or contact your insurance advisor to be properly prepared.

Review your policy limits and consider whether you might need additional insurance. Ask questions such as: Does my policy cover the cost to rebuild your home? Does it include additional living expenses (ALE), and if so, for what period of time?

If a disaster is declared for a specific region as a result of catastrophic damage, funding could be issued through FEMA for claims provided they fit within its requirements. However, funds are not guaranteed and likely would not be available immediately when you need them most.

Update Your Policy to Reflect Your Needs

To safeguard your belongings ahead of an unpredictable hurricane season, review your current policies and get with your insurance advisor to ensure you’re properly protected and prepared for whatever may come your way this season.

If you would like to find out more, request a quote online or speak to an IOA advisor today by calling (833) 546.2872.

For weather enthusiasts, find all storm names and their pronunciations here.

Saffir-Simpson Hurricane Scale

Written by

Bevrlee Lips

|June 1, 2025

Jump to section

01

A Mixed Bag of Predicted Activity

02

Now Is the Time to Review Your Coverage

03

Check the Details of Your Insurance Policy

04

Know Your Hurricane Deductible & Other Costs

05

Update Your Policy to Reflect Your Needs

06

Saffir-Simpson Hurricane Scale