Business insuranceInsightsRisk Management

The Softest Market Conditions Since 2017 Closes Out 2025

Written by: Bevrlee Lips | April 9, 2026

Jump to section

01

PREMIUM PRICE CHANGES – BY SIZE

02

PREMIUM PRICE CHANGES – BY LINE

03

NOTEWORTHY LINES

04

OUTLOOK

An overview of The Council of Insurance Agents & Brokers’ Commercial Property/Casualty Market Index Q4/2025 and marketing conditions ahead

Each quarter, The Council of Insurance Agents & Brokers releases its Commercial Property/Casualty Market Index. Here, we review the Q4 2025 findings, which utilize data from October 1 through December 31, 2025. We also consider current conditions to provide context for risk transfer solutions and strategic planning for emerging risks.

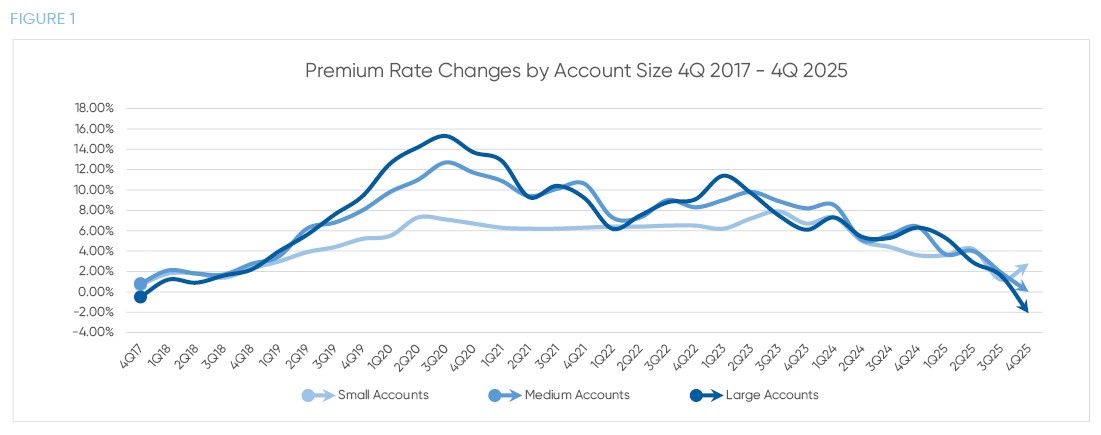

PREMIUM PRICE CHANGES – BY SIZE

The commercial insurance marketplace continued its transition into softer territory during Q4 2025. In stark contrast to average rate increases just five years earlier at 10.7% in 2020, average premium increases across all account sizes dropped to a minimal 0.2% in 4Q 2025, down from 1.6% in the previous quarter. This marked the 33rd consecutive quarter of average premium increases, but just barely, leaving people to ask, “Is the reign of the hard market over?”

Large account premiums decreased for the first time since Q4 2017, the end of the last soft market period recorded by the survey, coming in at an average of -2.1%. Medium accounts remained essentially flat with no premium movement, while small account premiums rose an average of 2.8%, up from 1.2% in Q3.

Respondents noted heightened competition among carriers, particularly for middle market and larger accounts. The increased appetite and capacity for these accounts drove more favorable pricing conditions. Conversely, the reason behind the uptick for small accounts was elusive, with some speculating that regional carriers appeared to be recalibrating their capacity and pulling back on limits to establish adequate rate levels before becoming more competitive in this segment.

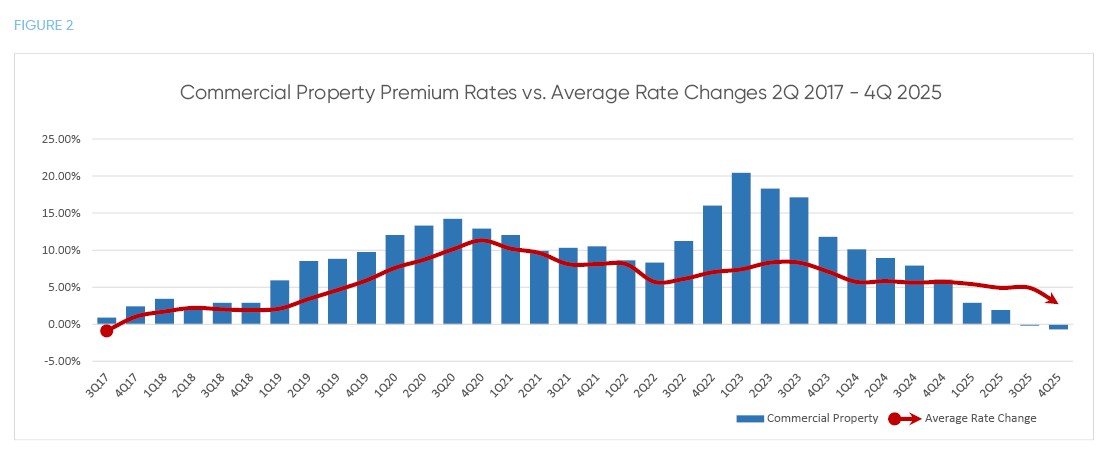

PREMIUM PRICE CHANGES – BY LINE

The soft market wave became even more pronounced when examining individual lines of business. More than half of all tracked lines—nine in total—posted premium decreases during Q4. These included business interruption, commercial property, construction, cyber, D&O, employment practices, surety bonds, terrorism, and workers compensation.

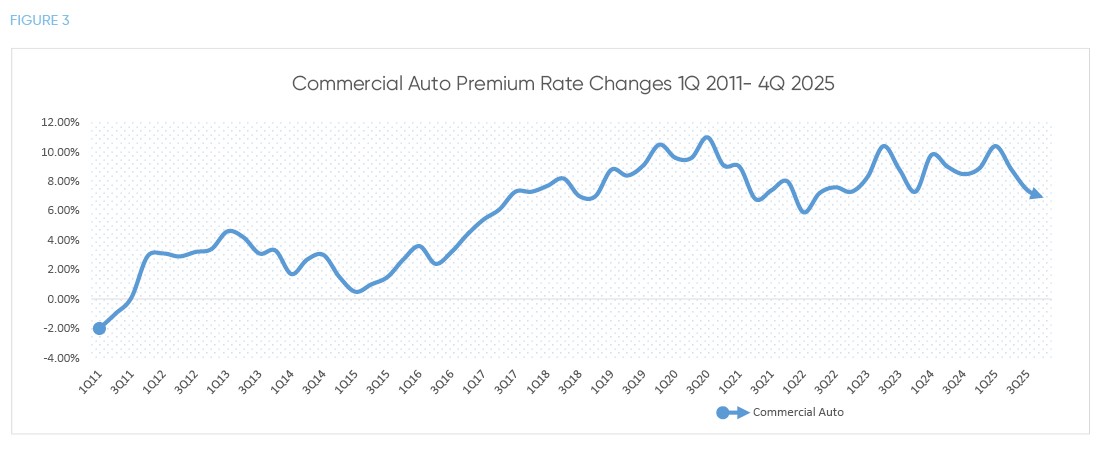

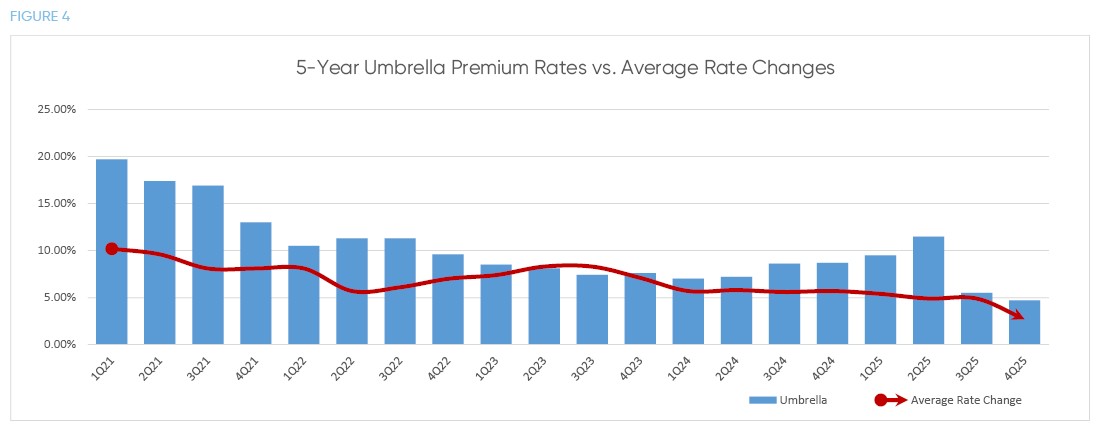

The five major coverage areas (commercial auto, commercial property, general liability, umbrella, and workers compensation) saw aggregate premium growth of just 1.9%, down from 2.7% in Q3. Only commercial auto and umbrella showed increases exceeding 2%, at 6.6% and 4.7% respectively.

NOTEWORTHY LINES

Commercial Property

Commercial Property

Property insurance continued to soften as 2025 came to an end with rates falling into negative territory for the second consecutive quarter. Reinforcing the softening trend, CRC Group’s Property REDY® Index Q4 2025 reported an average 87% of property account renewals in Q4 2025 experienced rate reductions.

Increased capacity and increased competition, which are inextricably tied together, provided the atmosphere for business owners to finally see meaningful rate reductions and improvements in coverage terms.

While market trends provided those improvements, we agree with Amwins’ statement in its State of the Market: 2026 Outlook, “Every renewal and new business opportunity should be reviewed on its own merits as every [business] has its own history and unique risk characteristics as well as its own advantages and challenges.” A strategic approach to achieving better rates in the future involves knowing your business inside and out. This is where your insurance advisor makes all the difference.

Commercial Auto

Commercial Auto

Commercial auto stands alone as the most persistently challenging line in the insurance market. Premium increases of 6.6% in Q4 marked more than 14 years, or 58 consecutive quarters, of uninterrupted rate growth dating back to mid-2011.

Capacity constraints intensified during Q4, with approximately 25% of survey participants reporting reduced underwriting appetite for this line. Industry sources also were aligned on claims frequency and severity trends as primary drivers, particularly losses tied to social inflation and expanding litigation costs.

According to Best’s Market Segment Report, “Stuck in Reverse: Commercial Auto Losses Keep Mounting,” average claim costs have more than doubled over the past decade, climbing at an average 8% annual rate, significantly outpacing the 3% economic inflation benchmark. The Institute for Legal Reform’s Tort Costs in America-Commercial Auto reported that tort costs surged from $33 billion in 2016 to $58 billion by 2022, representing a more than 10% compound annual increase. The steady and considerable uptick in total tort costs for commercial trucking and related transportation firms is demonstrably persistent.

Claims also remain open substantially longer than historical norms. The AM Best report notes that “insurers have more direct costs in attorney fees and expert witnesses as cases are negotiated before trial. Cases that remain open longer are potentially subjected to more impact from nuclear verdicts—directly in that the claim may be the nuclear verdict or indirectly in that a similar claim may result in a verdict that sets precedent in terms of amount.”

Umbrella

Umbrella

The umbrella market faces unique challenges stemming from its position in the coverage tower. When commercial auto claims breach primary policy limits—increasingly common with large verdicts—the excess layer absorbs the impact. This spillover dynamic has kept umbrella pricing relatively firm despite broader market softening.

Premium increases of 4.7% in Q4 reflect this ongoing pressure, though the rate of increase has moderated from earlier in the year when Q2 saw 11.5% growth. Industry observers attribute the umbrella challenge directly to commercial auto severity trends and the litigation environment.

According to a Marathon Strategies 2025 report, the nuclear verdict landscape remained active throughout the previous year, with 135 verdicts exceeding $10 million. Thermonuclear verdicts, or those over $100 million, hit an all-time record of 49 verdicts compared to 27 the previous year. Five of the thermonuclear verdicts surpassed $1 billion (name pending), compared to two the prior year. Many were concentrated in product liability, automotive and trucking, and intellectual property disputes.

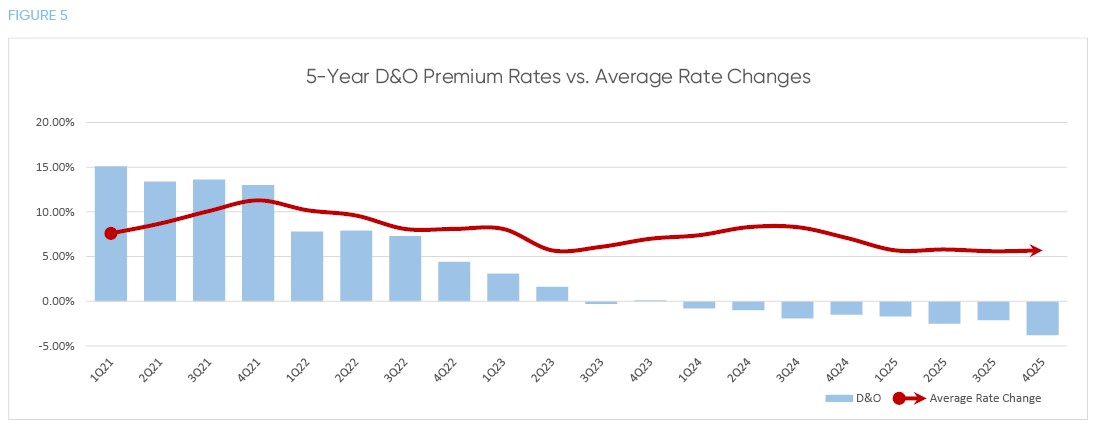

D&O

D&O

Directors and officers liability experienced its eighth consecutive quarterly decrease, with premiums falling 3.8%—the largest decline among all coverage lines. This sustained softening reflects three primary factors, according to the CIAB report: “more carriers, more capacity, and more competition.”

Approximately one-third of survey respondents noted increased underwriting capacity for D&O coverage. This abundance of available capital has intensified carrier competition for quality accounts. When multiple carriers compete for the same business, pricing naturally compresses.

The loss ratio story provides context for carrier willingness to compete aggressively. Best’s Market Segment Report, “Changing Environment Brings New Risks to D&O Insurers,” revealed that 2024 produced a 49% loss ratio for D&O—characterized as one of the best results in over a decade. This exceptional performance gave carriers confidence to pursue growth through competitive pricing rather than focusing solely on rate adequacy.

The industry also continues working through adverse development from soft market claims filed between 2016 and 2019, a headwind that may persist, while D&O underwriters simultaneously grapple with emerging AI-related exposures.

OUTLOOK

The commercial insurance market has clearly shifted into soft territory for the majority of coverage lines. Premium growth has slowed dramatically across all account segments, while more than half of tracked lines now show actual decreases—clear indicators of intensifying carrier competition.

Organizations should capitalize on this buyer-friendly environment to enhance coverage terms while maintaining robust risk management programs, as market cycles inevitably will shift.

In pursuit of the most favorable coverage terms, removing guesswork empowers clients and their experienced insurance brokers alike to negotiate competitively for better deliverables and better results.

Written by

Bevrlee Lips

|April 9, 2026

Jump to section

01

PREMIUM PRICE CHANGES – BY SIZE

02

PREMIUM PRICE CHANGES – BY LINE

03

NOTEWORTHY LINES

04

OUTLOOK