Business insuranceInsightsRisk Management

Focus Report – 2026 Transportation Market Outlook

Written by: Staff Writer | April 29, 2026

Jump to section

01

Depressed Volumes, Rising Premiums: Are There Any Bright Spots in Transportation?

02

TRENDS AND COSTS

03

WHY ARE INSURANCE RATES STILL RISING

04

NOTABLE FACTORS AND MITIGATION

05

ON THE HORIZON

06

THE VALUE OF AN EXPERT INSURANCE BROKER

Depressed Volumes, Rising Premiums: Are There Any Bright Spots in Transportation?

The transportation market is still suffering from high commercial auto costs, rising excess liability premiums, a prolonged period of reduced revenue and freight volume, and elevated risk of theft. But now we can add tariff challenges, changes to the Compliance, Safety, Accountability (CSA) program at the Federal Motor Carrier Safety Administration (FMCSA), and rapidly expanding cyberattacks.

The transportation market is still suffering from high commercial auto costs, rising excess liability premiums, a prolonged period of reduced revenue and freight volume, and elevated risk of theft. But now we can add tariff challenges, changes to the Compliance, Safety, Accountability (CSA) program at the Federal Motor Carrier Safety Administration (FMCSA), and rapidly expanding cyberattacks.

One potential risk of note is the U.S. Supreme Court case Montgomery v. Caribe Transport II LLC et al., which is expected to receive a decision this summer. The ruling will determine if brokers can be held liable for damages and injuries caused by a carrier that wasn’t vetted properly by the broker before being hired. A court ruling against C.H. Robinson, a named defendant in the case and largest freight brokerage in North America, would reframe insurance for freight brokers and motor carriers, who under current precedent have been protected from some state-level tort claims except when certain safety violations occur.

On the bright side, the number of large-truck crashes fell for the fourth straight year in 2025, according to FMCSA data, which also reported a third year of decline in large-truck fatal crashes. FMCSA projected another decline in large-truck crashes for 2025. Additionally, the number of miles traveled between breakdowns or unscheduled repairs improved slightly in 2024, according to the American Transportation Research Institute (ATRI), suggesting carriers may be taking preventive maintenance more seriously.

Another bright spot is a report from the American Trucking Associations (ATA) that the seasonally adjusted for-hire truck tonnage index for the first two months of 2026 rose 1.4% over the same period in 2025, which had recorded zero growth over 2024.

TRENDS AND COSTS

Financial pressures persist in the transportation industry. Deadhead mileage was up again in 2024 for non-tank runs, to 16.7% of non-tank miles traveled, according to ATRI. Adding to costly downtime, dwell time per stop rose slightly in 2024 in every sector except truckload dry van, which saw a 12-minute decrease to 1.48 hours per stop.

Financial pressures persist in the transportation industry. Deadhead mileage was up again in 2024 for non-tank runs, to 16.7% of non-tank miles traveled, according to ATRI. Adding to costly downtime, dwell time per stop rose slightly in 2024 in every sector except truckload dry van, which saw a 12-minute decrease to 1.48 hours per stop.

High operating costs and depressed freight rates caused overall adverse operating margins, some dramatic, in all trucking sectors, ATRI data show. Some fleets may be sidelining trucks due to a lack of drivers, a trend that has been worsening since 2020, according to ATRI data, which shows a 10-point drop in the driver-per-truck ratio, to 0.93 in 2024. ATRI says a ratio below 1.0 likely indicates a lack of financially viable freight.

That said, there is a tightening of capacity, with C.H. Robinson noting a “structurally smaller carrier base” for 2026, creating elevated load-to-truck ratios in some regions.

There also seems to be an increase in carrier discipline regarding rates, networks, and hiring.

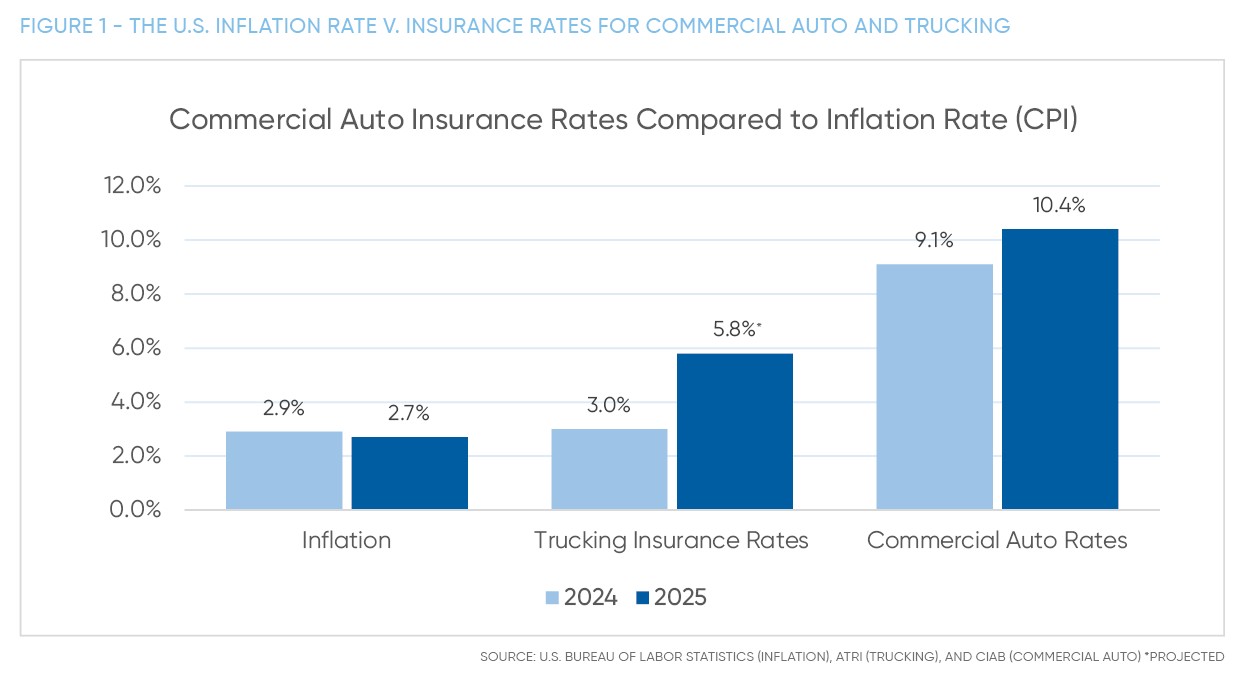

Truck insurance premiums rose to $0.102 per mile in 2024, ATRI data shows. That’s up 3% from the year before and 15.91% from 2022. ATRI’s Q1 2025 data indicated an overall year-over-year average premium change upward of 5.8% for the trucking sector broadly. The 3% increase, interestingly, is substantially below overall commercial auto rate hikes reported for 2024, which the Council of Insurance Agents & Brokers (CIAB) calculated at about 9.1%. And the projected 5.8% growth for Q1 2025 was far milder than the 10.4% overall average commercial auto increase the CIAB found in its Q1 Commercial Property/Casualty Market Index.

WHY ARE INSURANCE RATES STILL RISING

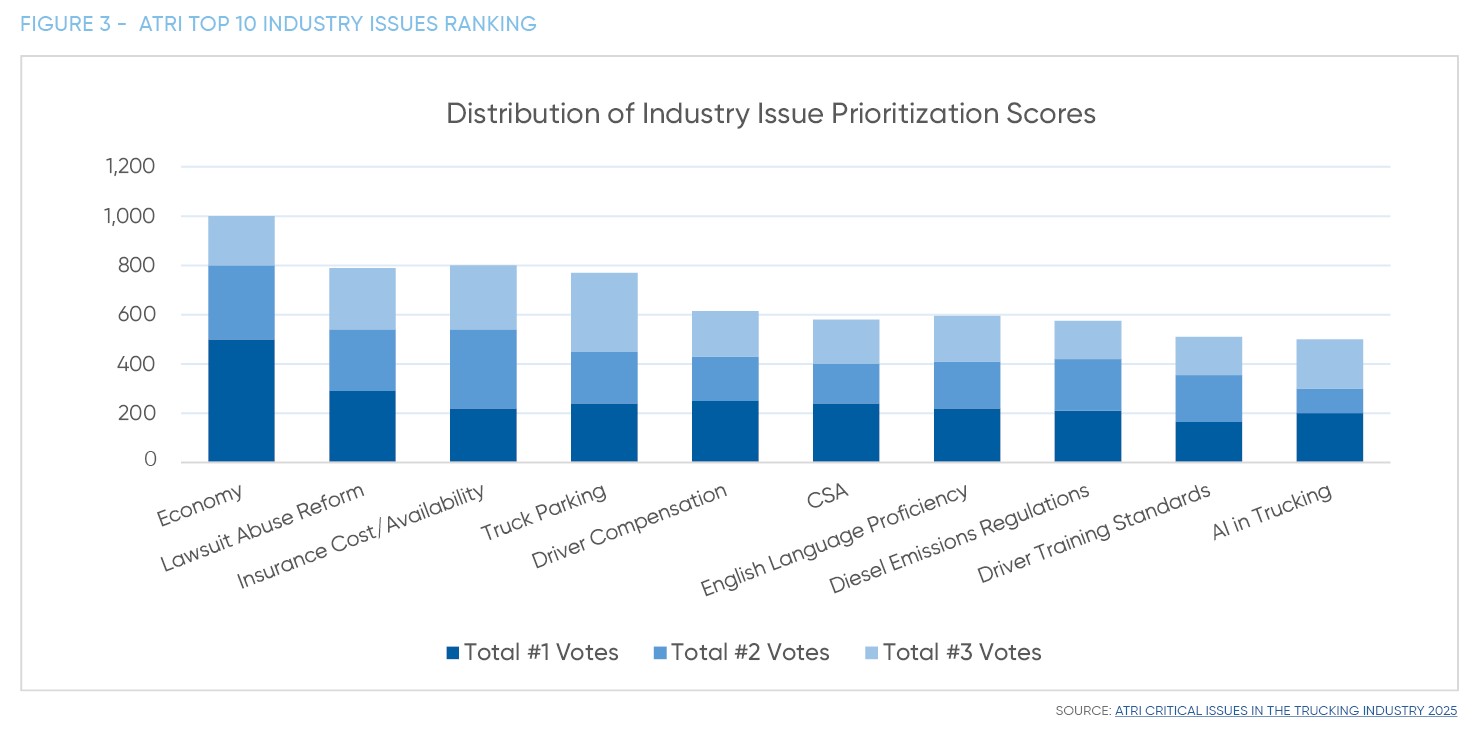

The differential between motor carrier insurance rates and overall averages across all commercial auto accounts probably reflects better accident data across the industry. Notwithstanding the moderation in premium growth, insurance costs rank third-highest in ATRI’s list of carrier concerns, and many fleet owners are lowering coverage limits and adopting higher deductibles. This can be an especially attractive option for larger companies or those with much lower risk than the norm.

The reduction in the number of insurance companies interested in covering the industry is putting upward pressure on premiums. Those that remain in the sector are restricting the type of trucks, cargo, and regions they’re willing to write.

Factors that are outside motor carriers’ and freight brokers’ control are also affecting insurance prices. Things such as high-value verdicts (sometimes called “nuclear” when above $10 million), insurers’ financial shortfalls elsewhere (such as from investment revenue), and anemic economic forecasts can all cause insurance companies to raise or hold rates at levels that don’t necessarily reflect the performance of individual policyholders.

Beyond those macro reasons, there are pressures from medical inflation, which includes about a 5.6% increase in hospital labor costs, 9.9% growth in fees for supplies, and 13.6% increase for pharmaceuticals in 2025, according to American Hospital Association data. In fact, AHA says higher input expense per patient accounts for 45% of the spike in the cost of care.

The cost of repairs is another driver of insurance premiums. From 2020 through 2025, total parts and labor pricing rose 27.4%, though Q4 2025 actually saw a cost decrease of 1.3%, according to the December 2025 Decisiv/TMC Parts and Labor Service Benchmark report. The increasing use of automation in trucks as well as escalating costs of steel and other materials suggest that repair costs will remain a significant factor in insurance premiums.

We noted above that the number of large-truck crashes has declined over the past four years and that the number of related fatalities has also been dropping. Nonetheless, ATRI estimates that about 11.8% of tractor-trailer accidents resulted in tort cases in 2022 (the latest data) and 3.8% of those (487 tort cases) are believed to have gone to trial, not having been settled or dismissed. Out of those 487, an estimated 313—or 64.3%—resulted in plaintiff victory, according to ATRI.

The organization emphasizes the value of moving to federal court where possible, stating that the median trial award in state courts was about $1.1 million higher than in federal courts.

NOTABLE FACTORS AND MITIGATION

While many risks confront the transportation industry, there are seven we want to highlight as particularly difficult challenges:

- Lawsuit abuse

- The claims process

- Alcohol/drugs/distracted driving

- Cyberrisk

- Tariff workarounds

- Parking

- English language proficiency

Each of these, however, is being addressed to the benefit of transportation firms.

Lawsuit abuse

Lawsuit abuse

Probably the most frustrating driver of liability insurance costs is lawsuit abuse. It is chronic, widespread, and escalating in frequency and severity. In ATRI’s 2025 Critical Issues report, lawsuit abuse reform was weighted second in priority of trucker concerns. ATRI cites third-party litigation funding, phantom damages (billed medical costs rather than actual amounts paid), and staged accidents as the top three problems in the legal arena, but forum shopping, where plaintiffs find the friendliest court venues, also is a significant issue.

There is little transportation companies can do to diminish lawsuit abuse, but one effective method we’ve seen is having vehicle camera footage that shows who was actually at fault in a crash. We encourage our clients to use 360o recording instead of just dashcams. This footage can reveal staged sideswipes and cut-in/sudden braking scams.

Lawsuit costs can be diminished if the case is moved from a plaintiff-friendly venue to federal court, so defense attorneys may issue that request where possible.

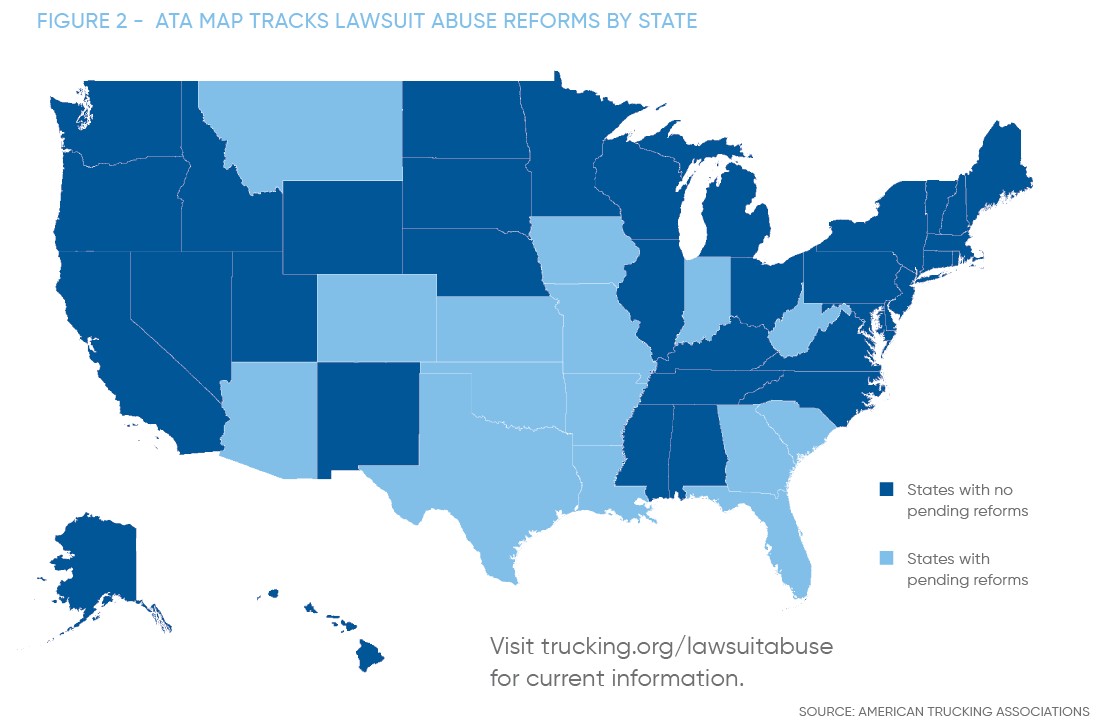

On the legislative side, several states are making progress on lawsuit abuse by eliminating phantom damages from compensation calculations or by making third-party litigation funding discoverable and reportable in lawsuits so juries know the actual financial beneficiaries of any award. The American Trucking Associations provide a map (Figure 2) that tracks lawsuit abuse reforms by state.

The claim process

Closely related to lawsuit abuse is the handling of accident claims. There are four tactics we have noted yielding positive results:

- Rapid response to claims

- Exterior-facing camera footage

- Learning management systems for drivers

- Diligence in driver selection

With a rapid response to a claim, the insurance company’s specialists can talk to a plaintiff before they get a lawyer involved and often present a pleasing settlement or sufficient evidence of fraud that the claim is disposed of without the chance for lawsuit abuse or outlandish jury awards.

By using exterior-facing cameras, drivers can provide their insurer recorded footage that can prove fraud and deter frivolous claims. Such footage also can help insurers decide when to settle and when to go to court to reveal dishonest claimants.

A learning management system (LMS) that is used to educate drivers can be an important element in a court decision on damages. Use of an LMS helps show seriousness about safety and training and can help prevent potentially harsh judgments.

Diligence in driver selection includes a motor vehicle record (MVR) review, verification of a legal commercial driver’s license, ongoing monitoring of driving records/violations, and employing a drug-testing protocol. The more a motor carrier can prove its conscientiousness regarding safety, the better it will fare in claims scenarios.

Alcohol/drugs/distracted driving

Last year we noted that 6% of fatal large-truck accidents involved drugs. According to the FMCSA’s 2022 crash facts report, that statistic remains the same. Distractions also remain a concern. At least one driver-related factor was involved in 33% of large-truck fatal accidents in 2022 (the latest data). Speeding was the top factor, with the careless driving, inattentive operation, improper driving, and driving without due care combined category ranking second for accidents involving carriers.

Inward-facing cameras (cabin cameras) have been touted as a solution to distracted driving; however, the industry has largely refused to install them partly due to driver complaints and partly due to the fact that they can muddy the waters in lawsuits. For example, a driver whose glance at a text message or reach for a soda corresponds to a cut-in/sudden brake accident could be blamed for what otherwise was a planned scam accident. In other words, correlation doesn’t equal causation, but it can be used against a motor carrier in court—even if it’s baseless.

Better solutions include random drug/alcohol testing, ignition interlocks, and quarterly reviews of MVRs.

Note that motor carriers are responsible for implementing successful U.S. Department of Transportation drug and alcohol programs under FMCSA 49 CFR Part 382 and/or DOT 49 CFR Part 40. You also must participate in the FMCSA Clearinghouse, a real-time database of CDL driver drug and alcohol violations. IOA transportation insurance brokers can assist with federal and state compliance so you are not alone when trying to navigate regulations.

Cyber claims

In our last report, we warned about the developing cyber crime industry with its efforts to reroute shipments, misdirect funds, and shut down services. The problems persist with the complicating enhancement of artificial intelligence, which enables cyber criminals to attack faster, smarter, and more broadly across all transportation networks.

AI makes determining where problems originate more difficult, and keeping up with the speed and agility of AI attacks has gotten more expensive and more complex. Personnel training is still the top priority to block scammers, but cyber criminals are so good that identifying false change orders or compromised vendor platforms is becoming impossible. The National Motor Freight Traffic Association’s 2026 Transportation Industry Cybersecurity Trends Report spotlighted API (application programming interface) security concerns as an elevated area of cyber criminal exploitation. These are the software programs that operate in the background to connect interactive platforms across the transportation industry. Compromise of an API would be virtually undetectable by the end user. Even GPS systems are being hacked.

The NMFTA says the most advanced carriers are using anomaly-detection software to spot deviations such as load cancellations and abnormal account-login patterns. With the professionalization of cyber crime, transportation companies also must up their investment in cyber defense.

One solution is cyberrisk insurance, which can be secured as third-party liability for others’ losses due to invasion of your system. But you also can get first-party cyber insurance that will help if your company experiences direct financial loss due to a cyber crime. Note that cyber coverage in a general liability policy may provide some aid, but it often falls far short of the limits needed for a significant event.

Tariff workarounds

With the U.S. tariffs on Canada, many Canadian motor carriers are creating U.S.-domiciled teams to get around tariff costs and red tape. IOA’s new partnership with Navacord has opened a convenient avenue for covering such companies, facilitating cross-border freight flows and travel. With this collaboration, we expect to be able to help Canadian carriers navigate the tariff landscape.

Parking shortages persist

ATRI’s survey puts parking at the fourth-highest concern of the transportation industry, an improvement over last year, but it is second-highest for drivers. Parking problems are a direct factor in cargo theft, but help is on the way. The FY2026 appropriations package President Trump signed in February contained a $200 million allocation solely for expansion of truck parking availability. In the meantime, truckers should take maximum efforts to minimize cargo theft opportunities and keep themselves safe during rest stops.

English language proficiency

An MC Advantage analysis of FMCSA data for small fleets showed that drivers with an English language deficiency had a 25% higher rate of accidents than drivers with a drug or alcohol violation. English deficiency was the top correlated factor in crash rates for midsize and large fleets as well.

The U.S. DOT was charged under the April 2025 Executive Order 14286 to change FMCSA rules to remove from service drivers who violate English language proficiency requirements. All motor carriers need to make sure they are compliant.

ON THE HORIZON

The biggest issue on the horizon is the Supreme Court’s decision in Montgomery v. Caribe Transport II LLC et al. The ruling will determine if there will still be a federal preemption for broker liability for damages caused by drivers the broker hired.

If the preemption is not upheld, we expect to see a patchwork of state rules that complicate insurance with tighter contracts for carriers, more carrier liability claims, higher insurance costs for brokers and carriers (potentially route dependent due to each state’s liability laws), and an outsized impact on smaller freight brokers. The decision is expected this summer, and IOA will follow up with an alert to clients on its effects. The U.S. Solicitor General filed an amicus brief favoring the federal exemption.

There have been some regulatory changes that all in the industry should be aware of. The U.S. Department of Transportation has committed to more aggressive enforcement of the top 10% of danger-causing driver-fitness violations under the CSA program, and CSA has up-weighted the value of recent violations, meaning recent violations will have a greater impact on your safety score. On the flip side, recent improvements will clean carrier records faster. CSA changes may necessitate a review of carrier protocols so you remain in compliance. CSA also is using a revised safety measurement system to reduce disadvantages to small fleets.

You may have heard a lot of talk about DOT removal of illegal drivers. It has been widely reported that a new DOT rule preventing non-citizens from obtaining commercial driver’s licenses will remove about 200,000 alien truck drivers from the roads over the next two years. We are watching these developments and will keep you advised of any impacts on driver/freight ratios as well as insurance rates and availability.

Lastly, we are continuing to follow the impacts of artificial intelligence on the industry. Its impacts go beyond the cybersecurity realm, potentially affecting freight brokers, motor carrier non-driver staff, insurance policy reviews/underwriting, and claims handling. As with any budding technology, we expect fits and starts along with some labor dislocation and unfamiliar (potentially glitchy) tech interface. We will do our best to monitor the situation and be transparent about any impacts we see affecting your insurance.

THE VALUE OF AN EXPERT INSURANCE BROKER

The transportation industry is rich with companies that all play important roles in the delivery of goods and people, but that makes it a complex field for risk management. An insurance broker with deep knowledge of motor carrier and freight broker risks and superior access to insurers that want to be in this space can help your transportation company reduce financial vulnerabilities and improve sustainability. Our in-house risk review and claims advocacy services complement our high reputation among insurance companies, allowing us to deliver excellence in transportation industry protection in the United States and for Canadian carriers with cross-border traffic. At IOA, we know your issues, will earn your trust, and look forward to providing the risk-reduction services you desire.

Written by

Staff Writer

|April 29, 2026

Jump to section

01

Depressed Volumes, Rising Premiums: Are There Any Bright Spots in Transportation?

02

TRENDS AND COSTS

03

WHY ARE INSURANCE RATES STILL RISING

04

NOTABLE FACTORS AND MITIGATION

05

ON THE HORIZON

06

THE VALUE OF AN EXPERT INSURANCE BROKER