Business insuranceInsightsRisk Management

The Hard Market Is Officially Over as Premium Increases Turn Negative

Written by: Bevrlee Lips | June 30, 2026

Jump to section

01

PREMIUM PRICE CHANGES – BY SIZE

02

PREMIUM PRICE CHANGES – BY LINE

03

NOTEWORTHY LINES

04

OUTLOOK

An overview of The Council of Insurance Agents & Brokers’ Commercial Property/Casualty Market Index Q1/2026 and marketing conditions ahead

Each quarter, The Council of Insurance Agents & Brokers releases its Commercial Property/Casualty Market Index. Here, we review the Q1 2026 findings, which utilize data from January 1 through March 31, 2026. We also consider current conditions to provide context for risk transfer solutions and strategic planning for emerging risks.

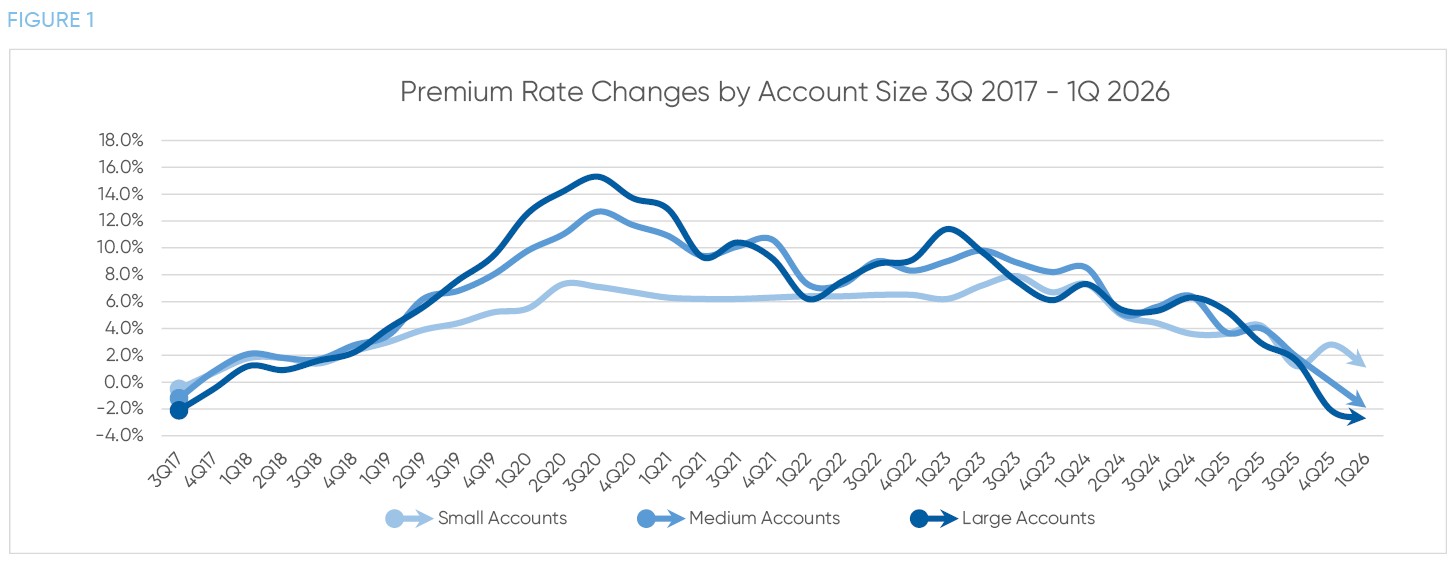

PREMIUM PRICE CHANGES – BY SIZE

The commercial insurance market crossed a meaningful threshold in Q1 2026 as the average premium across all account sizes declined for the first time since Q3 2017. The overall average landed at -1.2%, ending a 33-quarter streak of consecutive increases.

Large accounts saw the steepest decline at -2.7%, extending the negative trend that began last quarter. Medium accounts followed at -1.9%, while small accounts remained the lone exception, posting a modest increase of 1.1%, down from 2.8% in Q4. Respondents pointed to lower pricing, added flexibility in underwriting terms, and broader carrier appetite—potentially including risks that were declined at recent renewals—as hallmarks of the current environment.

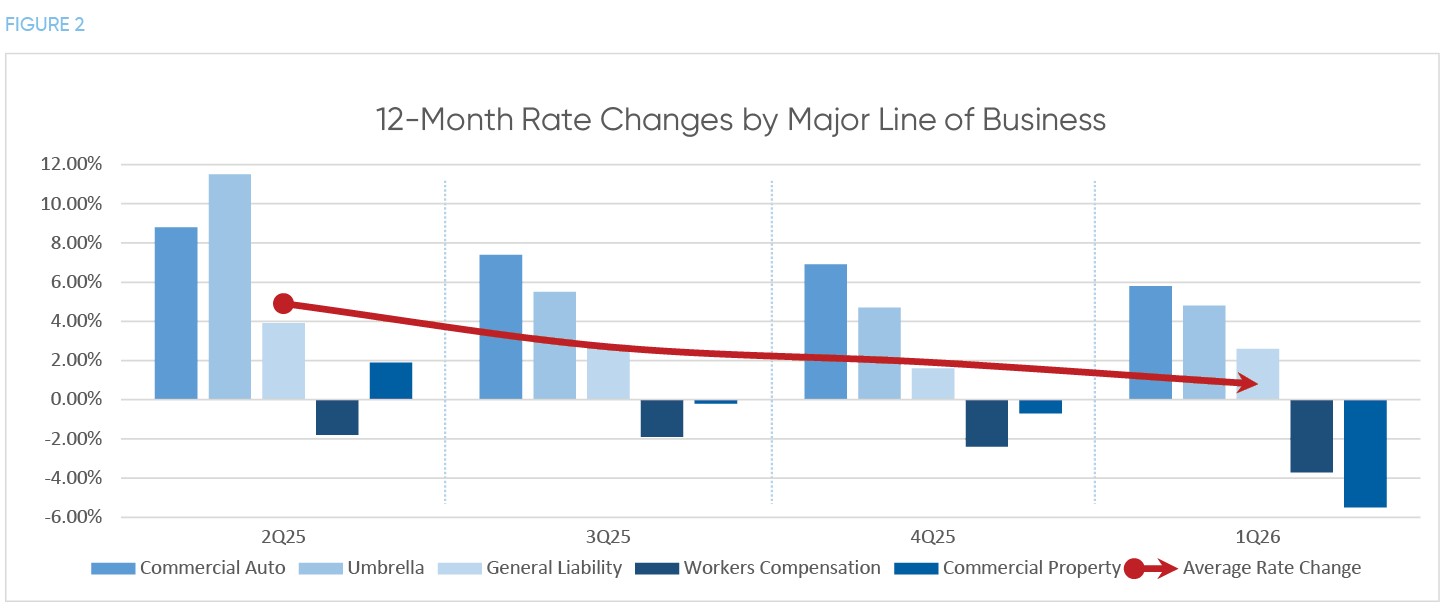

PREMIUM PRICE CHANGES – BY LINE

Soft market conditions were equally clear across lines of business. Nine lines posted premium decreases again in Q1, encompassing business interruption, commercial property, construction risks, cyber, D&O, employment practices, marine, terrorism, and workers compensation. For those lines with reported increases, half came in at around 1% or lower.

Soft market conditions were equally clear across lines of business. Nine lines posted premium decreases again in Q1, encompassing business interruption, commercial property, construction risks, cyber, D&O, employment practices, marine, terrorism, and workers compensation. For those lines with reported increases, half came in at around 1% or lower.

The average premium increase across all the major lines of business (commercial auto, commercial property, general liability, umbrella, and workers compensation) was just 0.8%, down from 1.9% in Q4 2025. When averaged across all tracked lines, premiums actually declined by 0.3%.

NOTEWORTHY LINES

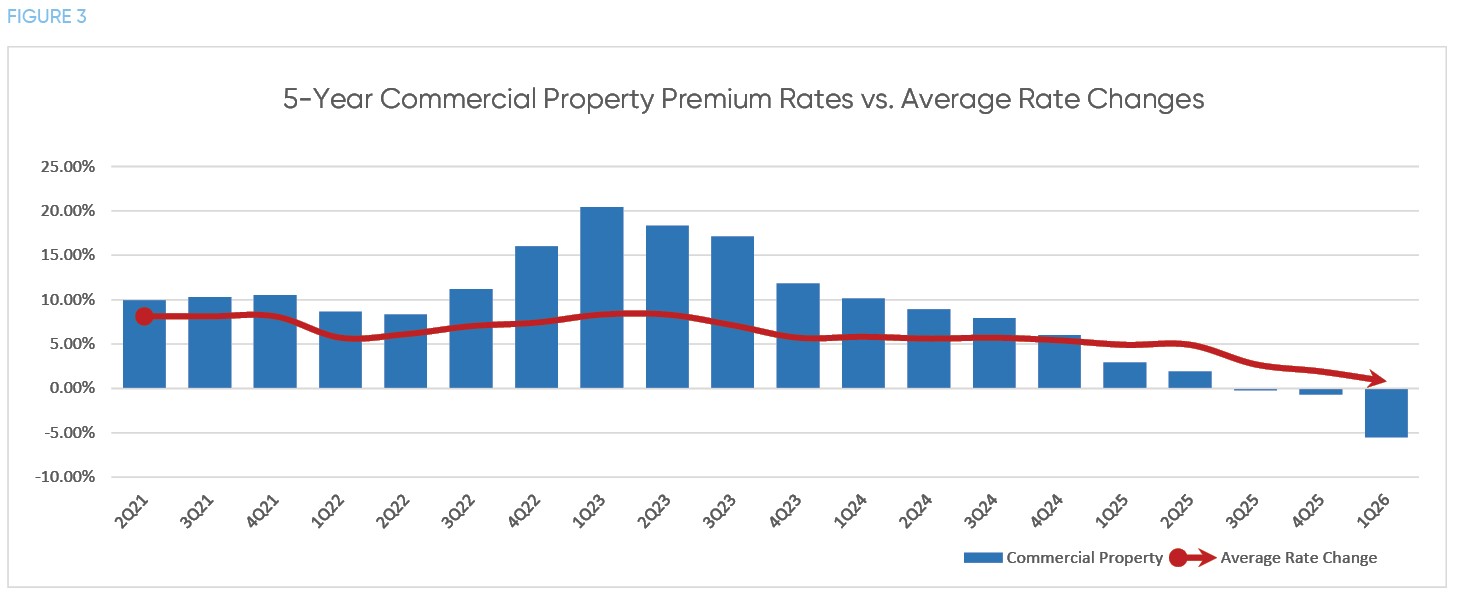

Commercial Property

Aggressive competition drove commercial property to its steepest decline in years with the largest rate drop of any line in Q1 2026. Premiums experienced a 5.5% average decrease, a significant acceleration downward from Q4’s -0.7%. This is a remarkable reversal from just three years ago when property premiums peaked at an average increase of 20.4% in Q1 2023.

Aggressive competition drove commercial property to its steepest decline in years with the largest rate drop of any line in Q1 2026. Premiums experienced a 5.5% average decrease, a significant acceleration downward from Q4’s -0.7%. This is a remarkable reversal from just three years ago when property premiums peaked at an average increase of 20.4% in Q1 2023.

Carrier appetite was described by multiple respondents as aggressive with widespread use of lower pricing and more favorable underwriting terms and conditions to compete for accounts. The greatest relief was seen in non-catastrophe-exposed property, even though some cat-exposed properties benefited from rate decreases or improved terms. Over 70% of respondents observed an increase in property underwriting capacity, some calling it “significant.”

Insight as to why carriers were feeling more comfortable easing pricing may be seen in AM Best’s March 2026 Market Segment Outlook. Despite early 2025 California wildfires and severe convective storm activity throughout the year, the annual loss ratio for commercial property improved from 87.9% at year-end 2024 to 85% at year-end 2025. AM Best attributed this improved profitability to disciplined capacity deployment, careful risk selection, and the robust premium base built during prior years of the hard market.

As was true in prior quarters, individual outcomes will continue to vary for commercial property owners. Geography, occupancy, construction type, and loss history all influence how competitive carriers will be on a given account. Working with an advisor who understands your risk profile and maintains strong carrier relationships remains essential to achieving the best possible result.

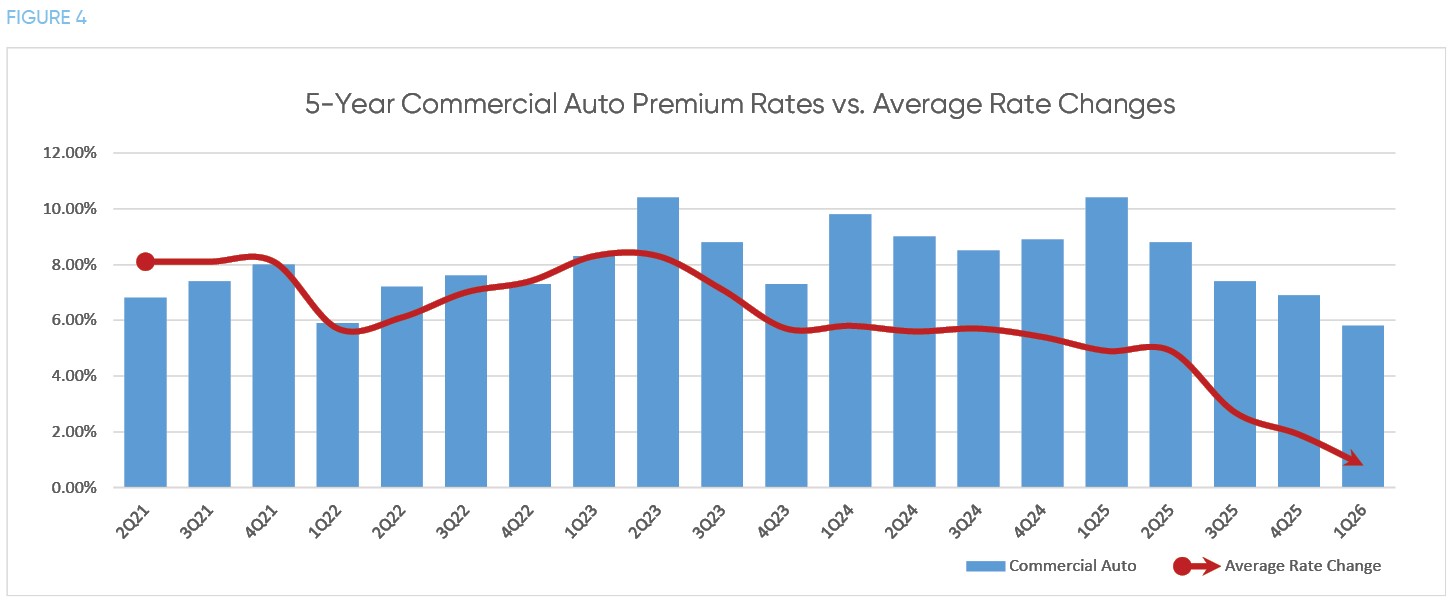

Commercial Auto

A nearly 15-year streak of premium increases shows no sign of ending. For the 59th consecutive quarter, commercial auto recorded the highest premium increase of all lines, averaging 5.8% in Q1 2026. As one respondent put it, “Auto premiums have eased, but remained problematic.” The slight moderation from Q4’s 6.6% is welcome, but the underlying drivers show little sign of abating.

A nearly 15-year streak of premium increases shows no sign of ending. For the 59th consecutive quarter, commercial auto recorded the highest premium increase of all lines, averaging 5.8% in Q1 2026. As one respondent put it, “Auto premiums have eased, but remained problematic.” The slight moderation from Q4’s 6.6% is welcome, but the underlying drivers show little sign of abating.

AM Best’s March 2026 Market Segment Outlook on U.S. Commercial Auto Insurance identified commercial auto as one of the worst-performing segments in the property/casualty industry over the past decade. Apart from 2021, the line has produced annual loss ratios above 100% every year since 2014, including loss ratios of 109.2% and 107.2% in 2023 and 2024, respectively, with net underwriting losses exceeding $5 billion in each of those years.

The culprits are well-established: distracted driving and congested roads contribute to high claim frequency, while social inflation and nuclear verdicts amplify severity far beyond what economic inflation alone would produce. Rising medical costs and the increased expense of repairing or replacing technologically complex vehicles add further pressure. Perhaps counterintuitively, the safety technology now standard in many vehicles—including telematics—has so far contributed to higher repair costs rather than lower ones, according to AM Best.

Smart risk management remains the most effective tool available to insureds. Telematics, driver behavior monitoring, route optimization, and documented safety programs all help demonstrate loss control commitment and can improve both pricing and coverage terms at purchase and renewal.

Moreover, telematics and other technologies may change insurance methodologies and, thereby, hyper-personalize commercial auto rates. For example, MarkWide Research stated in its May 2026 US Commercial Auto Insurance Market report, “Telematics-enabled usage-based rating models are compressing traditional underwriting cycles and forcing carriers to rebuild pricing architectures around real-time driver behavior rather than historical loss experience.”

OUTLOOK

Q1 2026 marked a genuine inflection point: the first quarter of average premium decreases across all account sizes in nearly nine years. The commercial insurance market has moved from hard to soft with a speed and breadth that has surprised many observers.

For most buyers, current conditions present a meaningful opportunity. Falling or flat rates across the majority of lines, combined with more flexible underwriting and broader carrier appetite, create an environment where coverage improvements—higher limits, reduced retentions, enhanced terms—may be achievable without significant premium impact.

That said, a few important considerations should inform how organizations approach this market:

The two-speed market is real. While property, cyber, workers compensation, and D&O have moved decisively in buyers’ favor, commercial auto and excess/umbrella remain under pressure. Organizations with significant auto exposure should not expect the same relief as those in lower-liability lines, and the spillover effect on umbrella means excess liability towers deserve careful attention.

Soft markets create temptation. The instinct to simply reduce premium spend can lead to coverage gaps that aren’t apparent until a claim occurs. Organizations may want to use this environment to strengthen their program rather than just reduce costs.

Every account is different. Averages tell a broad story, but individual outcomes depend heavily on loss history, geography, industry sector, and how well your risk is presented to the market. This is where an experienced advisor with deep carrier relationships can produce results that national averages can’t predict.

Cycles turn. The last soft market ended in Q4 2017. There is no telling when conditions will shift again, but they will. Organizations that use today’s environment to address coverage gaps and build strong carrier relationships will be better positioned when that shift occurs.

IOA remains committed to helping clients navigate this dynamic market with strategic guidance, clarity, and the deep carrier relationships that make a measurable difference at purchase and renewal.

Written by

Bevrlee Lips

|June 30, 2026

Jump to section

01

PREMIUM PRICE CHANGES – BY SIZE

02

PREMIUM PRICE CHANGES – BY LINE

03

NOTEWORTHY LINES

04

OUTLOOK